In the complex world of structured finance, securitization cusip bond accounting plays a critical role in tracking, reporting, and managing asset-backed securities. Securitization is a financial process where various types of financial assets—such as mortgages, auto loans, credit card receivables, or student loans—are pooled together and converted into tradable securities. These securities are then sold to investors in the form of bonds, and each bond is assigned a unique CUSIP number for identification and tracking. Proper accounting and reporting of these securities is essential for financial institutions, investors, auditors, and compliance professionals. This is where securitization cusip bond accounting becomes an important part of financial reporting and structured finance management.

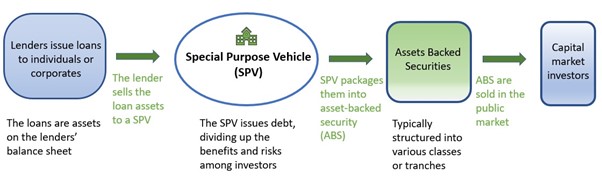

Securitization cusip bond accounting refers to the accounting, tracking, and reporting processes associated with bonds issued through securitization and identified by CUSIP numbers. A CUSIP (Committee on Uniform Securities Identification Procedures) number is a unique nine-character identifier assigned to financial instruments such as stocks and bonds. In securitization, each tranche of an asset-backed security is assigned a separate CUSIP, allowing investors and financial institutions to track payments, interest income, principal balances, and performance of each tranche individually. This level of tracking is essential because securitized bonds often have different risk levels, interest rates, and maturity dates depending on the tranche structure.

Asset-backed securities (ABS) and mortgage-backed securities (MBS) rely heavily on accurate accounting systems. Financial institutions must track cash flows from the underlying assets and allocate them correctly to each CUSIP bond holder. Securitization cusip bond accounting ensures that interest payments, principal repayments, servicing fees, and other financial transactions are recorded accurately and transparently. This process is not only important for internal accounting but also for investor reporting, regulatory compliance, and financial audits. Without proper accounting practices, institutions may face reporting errors, compliance issues, and financial discrepancies.

One of the most important aspects of securitization cusip bond accounting is cash flow allocation and bond balance tracking. When borrowers make payments on underlying loans, those payments are collected and distributed to investors according to the bond structure and payment waterfall. Accounting systems must accurately record these transactions and update bond balances associated with each CUSIP. This includes tracking interest income, principal reductions, prepayments, defaults, and losses. Accurate tracking ensures transparency and helps investors evaluate the performance of their investments.

Another critical component of securitization cusip bond accounting is financial reporting and compliance. Financial institutions must prepare detailed reports showing bond performance, outstanding balances, interest distributions, and payment histories. These reports are used by investors, auditors, and regulatory agencies to ensure compliance with financial regulations and accounting standards. Proper accounting also helps institutions maintain accurate financial statements and avoid regulatory penalties or reporting errors.

Technology and specialized accounting software are often used to manage securitization cusip bond accounting processes because of the large volume of transactions involved in securitized portfolios. These systems help automate payment tracking, reporting, reconciliation, and compliance documentation. Automation reduces errors, improves efficiency, and ensures accurate financial reporting across multiple CUSIP bonds and securitization deals.

In today’s structured finance industry, securitization cusip bond accounting is essential for managing asset-backed securities, ensuring accurate financial reporting, maintaining regulatory compliance, and providing transparency to investors. As securitization markets continue to grow and financial instruments become more complex, the importance of accurate CUSIP bond accounting will continue to increase. Financial institutions, auditors, and investors must understand these accounting processes to effectively manage securitized assets and ensure proper reporting and compliance in the structured finance environment.

The Role of CUSIP Numbers in Securitized Bonds

In the structured finance market, CUSIP numbers play a central role in identifying and tracking securities issued through securitization. Every bond issued in a securitization deal is assigned a unique CUSIP number, which helps investors, accountants, auditors, and financial institutions track specific bond tranches. Since securitized products are often divided into multiple tranches with different risk levels, interest rates, and maturity dates, the CUSIP number becomes the primary identifier used in accounting and reporting systems.

In securitization cusip bond accounting, each CUSIP represents a specific tranche of a securitized bond. Accounting teams use these identifiers to track interest payments, principal reductions, outstanding balances, and payment history. Without CUSIP-based tracking, it would be extremely difficult to manage large portfolios of asset-backed securities or mortgage-backed securities. CUSIP numbers ensure accuracy, transparency, and proper financial reporting across all securitized bond transactions.

Financial institutions also use CUSIP numbers for reconciliation and reporting purposes. When payments are received from underlying assets, those payments must be allocated to the correct bond tranches. Accounting systems rely on CUSIP numbers to ensure that payments are distributed accurately and recorded correctly in financial statements.

Cash Flow Allocation in Securitization Bond Accounting

Cash flow allocation is one of the most important components of securitization cusip bond accounting. In securitization, payments from underlying assets such as mortgages, auto loans, or receivables are collected and then distributed to investors based on a payment waterfall structure. This structure determines which bond tranches get paid first and which ones receive payments later.

Senior tranches usually receive payments first and have lower risk, while subordinate tranches receive payments later and carry higher risk but higher returns. Accounting for these payments requires accurate tracking of cash inflows and proper allocation to each CUSIP bond.

Accounting teams must record several types of transactions, including interest income, principal payments, prepayments, servicing fees, defaults, and losses. Each of these transactions must be allocated to the correct CUSIP bond. This process ensures that bond balances are updated correctly and that investors receive accurate payment reports.

Proper cash flow allocation is essential because errors in allocation can lead to financial reporting issues, investor disputes, and compliance problems. That is why securitization cusip bond accounting requires detailed tracking systems and reconciliation processes.

Bond Balance Tracking and Amortization

Another important aspect of securitization cusip bond accounting is bond balance tracking and amortization. As borrowers make payments on the underlying loans, the principal balance of the securitized bonds decreases over time. Accounting systems must track these principal reductions and update the outstanding balance for each CUSIP bond.

Bond amortization schedules are used to track how principal payments are applied over time. These schedules help accounting teams calculate remaining balances, interest payments, and expected maturity dates. Accurate amortization tracking is important for financial reporting, investor reporting, and portfolio valuation.

In many securitization structures, prepayments occur when borrowers pay off loans early. Prepayments affect bond balances and future interest income, so they must be recorded correctly in accounting systems. Securitization cusip bond accounting ensures that prepayments are applied to the correct bond tranches and that balances are updated accordingly.

Bond balance tracking also helps investors understand the performance of their investments and evaluate risk exposure. Accurate accounting records are essential for maintaining investor confidence and ensuring transparency in securitized bond portfolios.

Reporting Requirements for Asset-Backed Securities

Financial reporting is a major component of securitization cusip bond accounting. Financial institutions must generate detailed reports showing bond balances, interest payments, principal distributions, defaults, and losses. These reports are used by investors, auditors, and regulatory agencies.

Investor reports typically include payment history, outstanding bond balances, interest rates, and performance metrics for each CUSIP bond. These reports help investors track the performance of their investments and make informed decisions.

Regulatory reporting is also important in securitization accounting. Financial institutions must comply with accounting standards and regulatory requirements when reporting securitized assets and liabilities. Accurate securitization cusip bond accounting helps institutions meet these reporting requirements and avoid compliance issues.

Auditors also review securitization accounting records to ensure accuracy and compliance with accounting standards. Proper documentation, reconciliation, and reporting are essential for successful audits and financial transparency.

Reconciliation and Audit Processes in Securitization Accounting

Reconciliation is a critical process in securitization cusip bond accounting. Accounting teams must regularly reconcile cash flows, bond balances, interest payments, and principal payments to ensure that accounting records match trustee reports and investor reports.

Reconciliation involves comparing internal accounting records with external reports such as trustee statements, servicer reports, and investor distribution reports. Any discrepancies must be investigated and corrected to ensure accurate financial reporting.

Audit processes also play an important role in securitization accounting. Auditors review accounting records, payment allocations, bond balances, and financial reports to ensure compliance with accounting standards and financial regulations. Proper reconciliation and documentation help ensure that audits are completed successfully and that financial statements are accurate.

Without proper reconciliation and audit procedures, financial institutions may face reporting errors, compliance issues, or financial misstatements. This is why reconciliation is an essential part of securitization cusip bond accounting.

Technology and Software Used in CUSIP Bond Accounting

Due to the complexity and volume of transactions involved in securitization, most financial institutions use specialized software systems for securitization cusip bond accounting. These systems automate many accounting processes, including payment tracking, cash flow allocation, bond balance tracking, reporting, and reconciliation.

Accounting software helps reduce manual errors and improves efficiency in managing securitized bond portfolios. Automated systems can process large volumes of transactions quickly and generate detailed reports for investors and regulators.

Many institutions also use data management systems to track CUSIP numbers, bond structures, payment schedules, and performance metrics. These systems help accounting teams manage complex securitization deals and maintain accurate financial records.

Technology has significantly improved the efficiency and accuracy of securitization cusip bond accounting, making it easier for financial institutions to manage large securitized portfolios and comply with reporting requirements.

Importance of Compliance in Securitization Accounting

Compliance is a major concern in securitization and structured finance. Financial institutions must follow accounting standards, regulatory guidelines, and reporting requirements when managing securitized bonds. Securitization cusip bond accounting helps institutions maintain compliance by ensuring accurate tracking, reporting, and documentation.

Regulatory agencies require detailed reporting of securitized assets, bond balances, and cash flows. Accounting systems must maintain accurate records to support these reports. Failure to comply with regulations can result in penalties, legal issues, and financial reporting problems.

Compliance also involves maintaining proper documentation for securitization transactions, payment allocations, and accounting adjustments. Proper documentation ensures transparency and helps auditors verify financial records.

In structured finance, compliance and transparency are essential for maintaining investor confidence and ensuring the stability of financial markets. This is why accurate securitization cusip bond accounting is critical for financial institutions involved in securitization.

The Growing Importance of Securitization Bond Accounting

As the securitization market continues to grow, the importance of securitization cusip bond accounting is increasing. Financial institutions are managing larger portfolios of asset-backed securities, mortgage-backed securities, and structured finance products. Accurate accounting and reporting are essential for managing these portfolios and ensuring financial transparency.

Investors rely on accurate accounting reports to evaluate the performance of securitized bonds and make investment decisions. Auditors and regulators rely on accurate accounting records to ensure compliance and financial stability. Financial institutions rely on accurate accounting systems to manage cash flows, track bond balances, and prepare financial statements.

With increasing complexity in structured finance, accounting processes are becoming more sophisticated. Technology, automation, and data management systems are playing a larger role in managing securitization accounting processes.

In the modern structured finance industry, securitization cusip bond accounting is not just an accounting function but a critical part of financial reporting, compliance, investor reporting, and portfolio management. Institutions that maintain accurate and transparent accounting systems are better positioned to manage securitized assets, meet regulatory requirements, and maintain investor confidence in the structured finance market.

Conclusion

In the structured finance and asset-backed securities industry, securitization cusip bond accounting plays a vital role in ensuring accurate tracking, reporting, and financial transparency. From cash flow allocation and bond balance tracking to investor reporting and regulatory compliance, proper accounting practices are essential for managing securitized bonds effectively. Each bond tranche identified by a CUSIP number must be carefully monitored to ensure that interest payments, principal reductions, and outstanding balances are recorded accurately.

The importance of securitization cusip bond accounting continues to grow as securitization markets expand and financial instruments become more complex. Financial institutions, investors, auditors, and compliance professionals all rely on accurate accounting data to evaluate bond performance, prepare financial statements, and meet regulatory requirements. Without proper accounting systems and reconciliation processes, errors in reporting and payment allocation can create significant financial and compliance risks.

Ultimately, securitization cusip bond accounting is not just an accounting function but a critical component of structured finance operations. Accurate accounting ensures transparency, improves investor confidence, supports compliance, and helps financial institutions manage securitized portfolios efficiently in an increasingly complex financial environment.

Strengthen Your Cases with Expert Securitization & Forensic Audits

If you are looking to build stronger, more defensible cases backed by accurate securitization analysis and forensic audit research, we are here to support your success. For over four years, we have been helping our associates and partners uncover critical securitization data, identify reporting discrepancies, and provide detailed forensic audit support that strengthens case strategies and improves outcomes.

We are proud to operate exclusively as a business-to-business provider, working with professionals who require reliable securitization reports, CUSIP research, bond analysis, and forensic audit documentation. Our experience, accuracy, and commitment to detailed research help our associates present stronger, more informed cases with confidence.

Whether you need securitization chain analysis, CUSIP bond information, loan-level data research, or forensic audit support, our team is committed to delivering professional, accurate, and timely results to support your business and your clients.

Contact us today to learn how our securitization and forensic audit services can help you build stronger cases and better results for your clients.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”