In the complex world of structured finance, accurate tracking, reporting, and compliance are critical for investors, auditors, servicers, and financial institutions. One of the most important systems used in structured finance transactions is securitization cusip bond accounting, which plays a central role in identifying, tracking, and reporting securities throughout their lifecycle. Whether dealing with mortgage-backed securities, asset-backed securities, collateralized debt obligations, or other structured financial instruments, understanding how securitization cusip bond accounting works is essential for maintaining transparency and financial accuracy.

Securitization involves pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into tradable securities. These securities are then sold to investors in the capital markets. Each security issued through a securitization transaction is assigned a unique CUSIP number, which acts as a tracking identifier for the bond or security. This is where securitization cusip bond accounting becomes critical, as it ensures that every bond, tranche, and payment associated with the securitized asset is properly recorded, tracked, and reported.

CUSIP stands for Committee on Uniform Securities Identification Procedures, and the CUSIP number functions like a serial number for securities. In structured finance, there may be multiple tranches of securities issued from a single securitization trust, each with its own CUSIP number, interest rate, maturity date, and payment structure. Through securitization cusip bond accounting, financial professionals can monitor principal balances, interest payments, paydowns, defaults, and reporting requirements associated with each tranche of the securitized deal.

The importance of securitization cusip bond accounting extends beyond simple tracking. It is also essential for financial reporting, investor reporting, compliance, auditing, and forensic analysis. Servicers and trustees must maintain detailed records of cash flows, distributions, and bond balances tied to each CUSIP. Investors rely on these records to track their investments, calculate yields, and ensure they are receiving the correct payments. Auditors and forensic analysts use securitization cusip bond accounting to verify whether funds were properly allocated and whether securities were accounted for correctly within securitization structures.

Another major function of securitization cusip bond accounting is in bond accounting and reporting systems used by trustees, issuers, and institutional investors. These systems track amortization schedules, interest accruals, principal reductions, and outstanding bond balances associated with each CUSIP number. Because structured finance securities often involve complex payment waterfalls, priority structures, and tranche hierarchies, accurate accounting tied to each CUSIP is necessary to ensure proper distribution of funds.

In addition, securitization cusip bond accounting is widely used in compliance and regulatory reporting. Financial institutions must maintain accurate bond accounting records to comply with accounting standards, regulatory requirements, and investor reporting obligations. Proper CUSIP-based accounting ensures transparency in structured finance transactions and helps prevent reporting errors, accounting discrepancies, and compliance issues.

For forensic audits and securitization reviews, securitization cusip bond accounting can also help identify discrepancies between loan pools, securities issued, and payments distributed to investors. Analysts often use CUSIP numbers to trace securities through securitization trusts, investor reports, and bond payment histories. This process helps determine whether securitized assets were properly transferred, accounted for, and reported throughout the life of the securitization.

Understanding securitization cusip bond accounting is therefore essential for anyone involved in structured finance, including auditors, accountants, financial analysts, investors, mortgage professionals, and securitization specialists. From tracking securities and recording bond balances to ensuring compliance and conducting forensic audits, CUSIP-based bond accounting is a foundational component of modern structured finance operations.

In this ultimate guide, we will explore how securitization cusip bond accounting works, how CUSIP numbers are used in structured finance, how bond accounting is performed for securitized securities, and how financial professionals track and report securitization bonds using CUSIP-based accounting systems.

Understanding the Role of CUSIP Numbers in Structured Finance

In structured finance, the entire securitization process depends heavily on identification, tracking, and reporting of securities issued from pooled financial assets. This is where securitization cusip bond accounting becomes a fundamental part of financial management and reporting. Every bond or tranche issued in a securitization transaction is assigned a unique CUSIP number, which allows financial institutions, trustees, investors, and auditors to track each security separately. Since securitization deals often include multiple tranches with different interest rates, maturities, and payment priorities, accurate identification through CUSIP numbers is essential for proper bond accounting.

The CUSIP number acts as a unique identifier similar to a serial number for financial securities. In securitization transactions such as mortgage-backed securities (MBS) or asset-backed securities (ABS), dozens or even hundreds of securities may be issued under a single securitization trust. Through securitization cusip bond accounting, each of these securities is tracked individually, ensuring accurate reporting of principal balances, interest payments, and outstanding bond amounts. Without this system, it would be extremely difficult to manage structured finance transactions and maintain accurate financial records.

How Securitization Bond Accounting Works

To understand securitization cusip bond accounting, it is important to first understand how bond accounting works within securitization structures. When loans are pooled and securitized, securities are issued to investors in different tranches. Each tranche has its own CUSIP number and payment structure. The accounting process tracks how cash flows from the underlying loans are distributed to investors holding each tranche.

Bond accounting in securitization includes several key components such as interest accrual, principal payments, bond balance tracking, amortization, and payment distribution. Every month, payments collected from borrowers are allocated through a payment waterfall. These payments are then recorded under each CUSIP number through securitization cusip bond accounting systems. The accounting records show how much principal has been paid down, how much interest has been paid, and what the remaining bond balance is for each CUSIP.

This process ensures transparency and allows investors to monitor the performance of their investments. Trustees and servicers rely on securitization cusip bond accounting to generate investor reports, financial statements, and compliance reports related to securitized bonds.

Tracking Principal and Interest Payments Using CUSIP Bond Accounting

One of the most important functions of securitization cusip bond accounting is tracking principal and interest payments associated with each security. In structured finance transactions, borrowers make monthly payments that include both principal and interest. These payments are collected by servicers and then distributed to investors according to the payment waterfall structure defined in the securitization agreement.

The accounting system records these payments under each CUSIP number. For example, if a securitization trust issued multiple tranches such as senior bonds, mezzanine bonds, and subordinate bonds, each tranche would have its own CUSIP number. The securitization cusip bond accounting system tracks how much payment each tranche receives, how much principal is reduced, and what the remaining outstanding balance is.

This level of detailed tracking is essential for investor reporting and financial transparency. Investors rely on these records to calculate yields, monitor bond performance, and track outstanding balances. Without proper securitization cusip bond accounting, it would be impossible to maintain accurate payment records for structured finance securities.

Investor Reporting and Financial Reporting Requirements

Investor reporting is another major area where securitization cusip bond accounting plays a critical role. Trustees and servicers must prepare monthly or quarterly investor reports that show bond balances, interest payments, principal distributions, and remaining outstanding amounts for each CUSIP. These reports are used by investors, rating agencies, auditors, and regulators.

The investor reports typically include beginning bond balance, principal payments received, interest payments distributed, ending bond balance, and cumulative losses if any. All of this information is generated through securitization cusip bond accounting systems that track each security individually.

Financial reporting also depends on accurate bond accounting records. Companies that hold securitized bonds must report their investments on financial statements, including balance sheets and income statements. Accurate accounting tied to CUSIP numbers ensures that financial statements reflect correct investment balances and income earned from securitized bonds.

Compliance, Auditing, and Regulatory Requirements

Compliance and auditing are major reasons why securitization cusip bond accounting is so important in structured finance. Financial institutions must comply with accounting standards, regulatory requirements, and reporting obligations. Accurate bond accounting records tied to CUSIP numbers help ensure compliance with these requirements.

Auditors often review securitization cusip bond accounting records to verify that securities are properly recorded, payments are accurately distributed, and bond balances are correctly reported. Forensic audits may also use CUSIP bond accounting records to trace securities through securitization transactions and verify whether assets were properly transferred into securitization trusts.

Regulators may also review securitization bond accounting records to ensure transparency and proper reporting of structured finance transactions. Proper securitization cusip bond accounting helps prevent accounting errors, reporting discrepancies, and compliance violations.

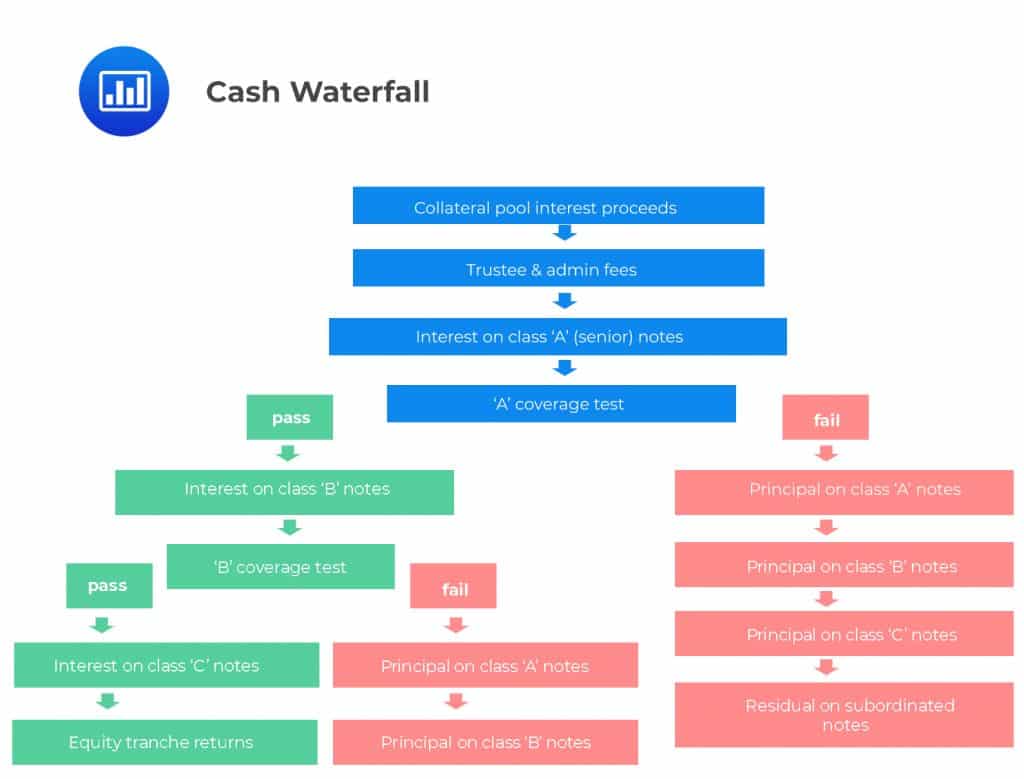

Payment Waterfalls and Tranche Accounting

Structured finance securities operate under payment waterfall structures, which determine how cash flows are distributed among different tranches of securities. Senior tranches are paid first, followed by mezzanine tranches and then subordinate tranches. Each tranche has its own CUSIP number and accounting records.

Through securitization cusip bond accounting, accountants track how payments move through the waterfall and how much each tranche receives. The accounting system records interest payments, principal paydowns, losses, and remaining balances for each tranche separately.

This process is critical because structured finance securities often have complex payment structures. Some tranches may receive interest only, some may receive principal and interest, and others may receive payments only after senior tranches are fully paid. Accurate securitization cusip bond accounting ensures that all payments are properly recorded and distributed according to the securitization agreement.

Common Challenges in Securitization CUSIP Bond Accounting

Despite its importance, securitization cusip bond accounting can be complex and challenging due to the nature of structured finance transactions. One of the biggest challenges is tracking multiple tranches and CUSIP numbers within a single securitization deal. Each tranche may have different payment schedules, interest rates, and amortization structures.

Another challenge is reconciling investor reports, trustee reports, and accounting records. Sometimes discrepancies may arise between reported bond balances and accounting records. In such cases, detailed securitization cusip bond accounting analysis is required to reconcile differences and identify the source of discrepancies.

Loan defaults, prepayments, and losses also add complexity to securitization bond accounting. When loans default or are prepaid, the cash flow structure changes, and bond balances must be adjusted accordingly. Accurate accounting systems are necessary to track these changes and ensure that bond balances remain accurate.

Importance of Accurate Record Keeping in Structured Finance

Accurate record keeping is the foundation of securitization cusip bond accounting. Every payment, adjustment, balance change, and distribution must be recorded accurately under the correct CUSIP number. These records are used for investor reporting, financial reporting, compliance, auditing, and forensic analysis.

Poor record keeping can lead to accounting errors, reporting discrepancies, compliance issues, and investor disputes. This is why financial institutions invest heavily in accounting systems and reporting systems designed specifically for securitization bond accounting.

Accurate securitization cusip bond accounting also helps in tracking bond performance, calculating yields, monitoring outstanding balances, and ensuring that payments are distributed correctly according to securitization agreements.

The Future of Securitization CUSIP Bond Accounting

As structured finance markets continue to evolve, securitization cusip bond accounting will continue to play a crucial role in financial reporting, compliance, and investor transparency. With increasing regulatory requirements and reporting standards, accurate bond accounting tied to CUSIP numbers is becoming even more important.

Technology and automation are also changing the way securitization bond accounting is performed. Modern accounting systems and structured finance reporting platforms now automate many aspects of bond accounting, including payment tracking, interest accruals, principal tracking, and investor reporting. These systems reduce errors and improve efficiency in securitization cusip bond accounting processes.

In the future, securitization markets may rely even more on automated reporting, blockchain tracking systems, and advanced analytics to improve transparency and tracking of securitized securities. However, the core principle of securitization cusip bond accounting will remain the same: tracking, reporting, and accounting for securities using unique CUSIP identifiers to ensure accuracy, transparency, and compliance in structured finance transactions.

Conclusion

In the world of structured finance, accurate tracking, reporting, and compliance are essential for managing complex securities and investment structures. This is where securitization cusip bond accounting plays a critical role. By assigning unique CUSIP identifiers to each bond or tranche issued in a securitization transaction, financial institutions, trustees, and investors can accurately track principal balances, interest payments, amortization, and outstanding bond amounts throughout the life of the security. Without proper securitization cusip bond accounting, it would be extremely difficult to manage investor reporting, financial reporting, and regulatory compliance in structured finance transactions.

Another important aspect of securitization cusip bond accounting is transparency. Investors rely on accurate bond accounting records tied to CUSIP numbers to monitor investment performance, track payments, and evaluate risk exposure. Auditors and forensic analysts also use securitization cusip bond accounting to verify the accuracy of securitization transactions, payment distributions, and bond balances. This makes CUSIP-based bond accounting not only an accounting function but also a compliance and risk management tool.

As structured finance markets continue to grow and evolve, the importance of securitization cusip bond accounting will continue to increase. Accurate accounting, reporting, and tracking systems tied to CUSIP numbers will remain essential for maintaining transparency, compliance, and investor confidence in securitized financial markets.

Build Stronger Cases with Expert Securitization & Forensic Audit Support

For over four years, Mortgage Audits Online has been a trusted partner for professionals who need accurate, detailed, and reliable securitization and forensic audit support. We specialize exclusively in business-to-business services, helping attorneys, auditors, financial professionals, and consultants build stronger, evidence-backed cases with confidence and clarity.

Our team understands the complexities of securitization, CUSIP research, bond tracking, and forensic loan analysis. That’s why we focus on delivering precise, well-documented audit reports that help our associates uncover critical information, support litigation, strengthen negotiations, and improve case strategies. When accuracy and documentation matter, having the right audit partner can make a significant difference in the outcome of your case.

If you are looking for a professional team that understands structured finance, securitization, and forensic auditing, Mortgage Audits Online is ready to support your business with reliable and professional services tailored for industry professionals.

Contact us today to learn how our securitization and forensic audit services can help you build stronger, more effective cases.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”