In today’s complex financial environment, structured finance and mortgage-backed securities have become essential components of institutional investing, banking, and loan servicing operations. One of the most critical yet often misunderstood areas within structured finance is securitization cusip bond accounting. Financial professionals, auditors, forensic analysts, and compliance officers must understand how securitized loans are tracked, reported, and accounted for using CUSIP identifiers to ensure transparency, compliance, and accurate financial reporting. Without proper accounting procedures, institutions may face reporting errors, compliance risks, and financial misstatements.

Securitization cusip bond accounting refers to the accounting, tracking, and reporting of bonds created through securitization processes, where loans such as mortgages, auto loans, or receivables are pooled together and converted into tradable securities. Each security issued in the securitization process is assigned a unique CUSIP number, which acts as an identifier for tracking ownership, payments, transfers, and reporting in financial statements. These CUSIP-linked securities must be properly recorded in accounting systems to ensure accurate balance sheet reporting, interest income recognition, and investor reporting.

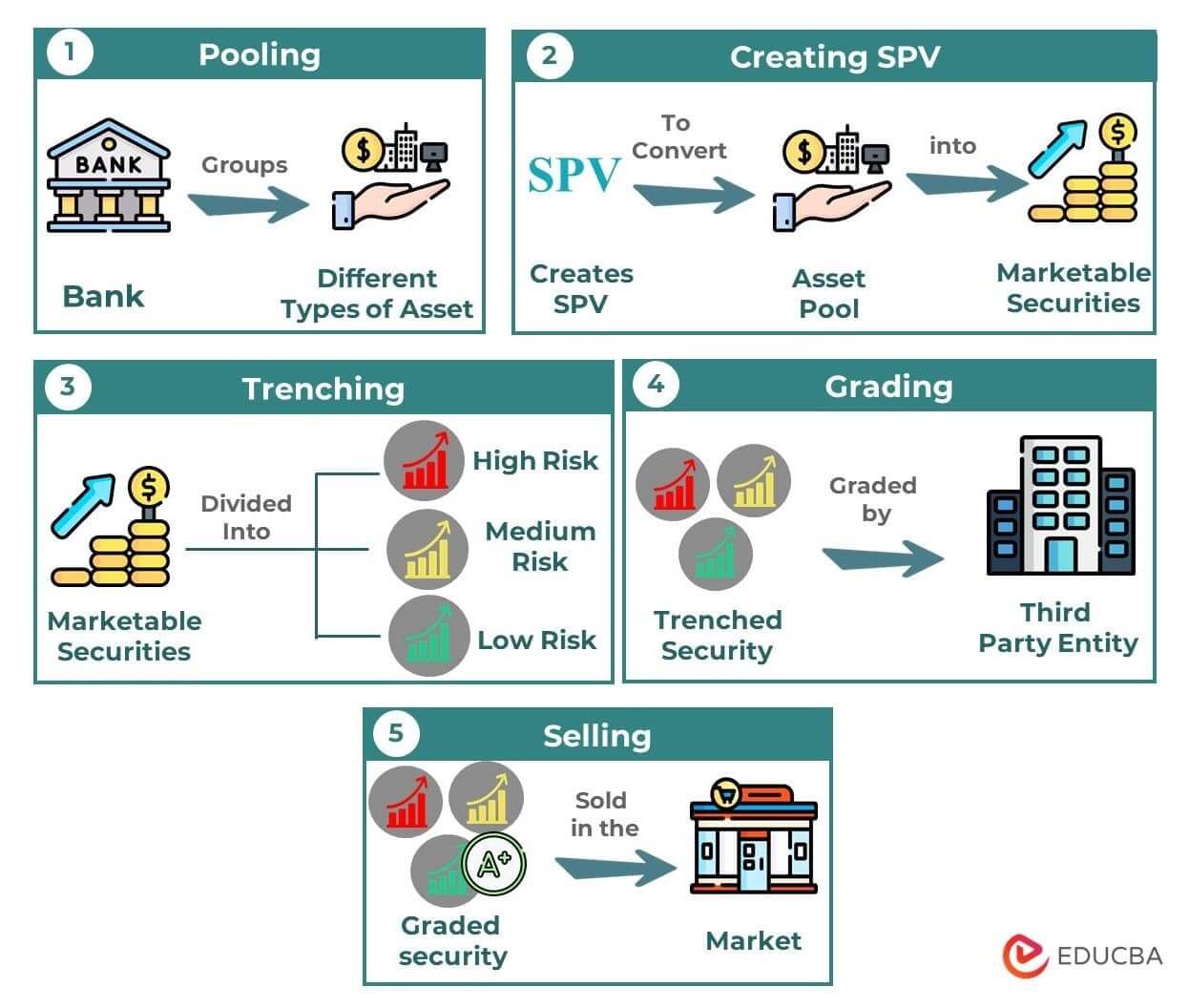

The securitization process begins when financial institutions pool loans and transfer them into a trust or special purpose vehicle (SPV), which then issues bonds to investors. These bonds are assigned CUSIP numbers and sold in the secondary market. From an accounting perspective, this process involves loan removal from the originator’s balance sheet, recognition of sale or financing treatment, recording of servicing assets, and ongoing tracking of bond performance. This is where securitization cusip bond accounting becomes essential, as each bond tranche must be tracked separately for principal payments, interest income, amortization, and reporting.

For financial professionals, understanding securitization cusip bond accounting is important not only for bookkeeping but also for compliance with accounting standards such as GAAP, IFRS, and regulatory reporting requirements. Proper accounting ensures that income is recognized correctly, assets and liabilities are properly classified, and investors receive accurate reports. In securitized structures, multiple tranches may exist with different risk levels, interest rates, and maturity dates, making accounting more complex than traditional bond accounting.

Another important aspect of securitization cusip bond accounting is reconciliation and tracking. Financial institutions must reconcile loan pools with issued securities, track cash flows from borrowers to investors, record servicing fees, and ensure that principal and interest distributions match the bond payment structure. This requires detailed accounting systems and accurate CUSIP-level tracking to prevent discrepancies and reporting errors.

Additionally, forensic accounting and audit professionals often review securitization cusip bond accounting records to verify loan ownership, transfer history, and investor reporting accuracy. In mortgage securitization audits, analysts frequently trace loans through CUSIP numbers to determine whether loans were properly transferred into trusts and whether securities were correctly issued and reported. This makes CUSIP bond accounting not only an accounting function but also a critical part of financial transparency and audit verification.

As securitization markets continue to grow and financial instruments become more complex, the importance of accurate securitization cusip bond accounting continues to increase. Financial professionals must understand the step-by-step accounting process, from loan securitization and bond issuance to ongoing reporting, reconciliation, and compliance. Proper accounting practices ensure transparency, regulatory compliance, accurate financial reporting, and investor confidence in securitized financial instruments.

In the following sections, financial professionals will learn the step-by-step process of securitization CUSIP bond accounting, including loan pooling, bond issuance, accounting entries, reporting procedures, and compliance requirements. Understanding these steps is essential for accountants, auditors, financial analysts, and securitization professionals working in structured finance and bond accounting environments.

Understanding the Structure of Securitization Before Accounting Begins

Before professionals can properly perform securitization cusip bond accounting, it is essential to understand the structure of securitization itself. Securitization is the process of pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into tradable securities that investors can purchase. These securities are issued through a special purpose vehicle (SPV) or trust, which holds the pooled assets and distributes income to investors.

In a typical securitization structure, the originator sells a pool of loans to the trust, and the trust issues bonds in different tranches. Each tranche represents a different level of risk and return. Senior tranches are paid first and are considered lower risk, while junior or subordinate tranches carry higher risk but offer higher returns. Each tranche issued is assigned a unique CUSIP number, which is used for tracking, reporting, and accounting purposes. This is where securitization cusip bond accounting becomes important because each CUSIP represents a specific security that must be tracked separately in accounting records.

Financial professionals must understand that accounting in securitization is not just about recording a bond purchase or sale. It involves tracking loan pools, bond issuance, interest income, principal payments, servicing fees, and investor distributions. Proper accounting ensures transparency and accurate financial reporting throughout the life of the securitization.

Loan Pool Transfer and Initial Accounting Entries

The first major accounting step in securitization cusip bond accounting occurs when loans are transferred from the originator to the securitization trust or SPV. This transfer may be treated either as a sale or as a secured borrowing, depending on accounting standards and whether control of the assets has been legally transferred.

If the transfer qualifies as a sale, the originator removes the loans from its balance sheet and records cash received from the trust. The originator may also record a gain or loss on sale and recognize a servicing asset if it continues to service the loans. If the transfer is treated as a financing transaction, the loans remain on the originator’s balance sheet and a liability is recorded for the funds received.

This stage is critical in securitization cusip bond accounting because the accounting treatment determines how assets, liabilities, and income are reported in financial statements. Incorrect classification can lead to financial reporting errors and compliance issues.

Once the loans are transferred into the trust, the trust issues securities to investors. Each security issued is assigned a CUSIP number, and accounting records must be created for each CUSIP separately. These records will track principal balances, interest rates, payment schedules, and investor distributions.

Recording Bond Issuance and CUSIP-Level Tracking

After the loan pool is transferred into the trust, bonds are issued to investors. Each bond tranche receives a unique CUSIP identifier. The accounting team must create individual accounting records for each CUSIP because each tranche may have different interest rates, maturity dates, and payment priorities.

In securitization cusip bond accounting, the bond issuance is recorded as a liability on the trust’s books. The proceeds from investors are recorded as cash, while the issued bonds are recorded as liabilities under each CUSIP. This allows financial professionals to track each tranche separately.

CUSIP-level tracking is extremely important because principal and interest payments are distributed according to tranche priority. Senior bondholders are paid first, followed by mezzanine and subordinate bondholders. Accounting systems must track these payments accurately to ensure proper reporting and investor distributions.

Over time, principal payments from borrowers reduce the outstanding bond balances. Interest payments are recorded as interest expense for the trust and interest income for investors. All of these transactions must be recorded at the CUSIP level as part of securitization cusip bond accounting procedures.

Interest Income Recognition and Cash Flow Allocation

One of the most important parts of securitization cusip bond accounting is the recognition of interest income and allocation of cash flows. Borrowers make monthly payments that include both principal and interest. These payments are collected by the loan servicer and then distributed to investors based on the payment structure defined in the securitization agreement.

The accounting team must allocate cash flows in the following order:

Servicing fees

Trust expenses

Interest payments to bondholders

Principal payments to bondholders

Residual payments to equity or subordinate investors

Each of these allocations must be recorded accurately in accounting records. Interest income must be recognized based on the effective interest rate of each bond tranche. Principal payments reduce the bond liability balance associated with each CUSIP.

Accurate cash flow allocation is essential in securitization cusip bond accounting because errors in allocation can lead to incorrect investor reporting and financial statement misstatements. Financial professionals must reconcile borrower payments, servicer reports, and investor distributions regularly to ensure accuracy.

Amortization, Principal Reduction, and Bond Balance Tracking

Another major component of securitization cusip bond accounting is tracking bond amortization and principal reduction. As borrowers make payments, part of each payment goes toward reducing the principal balance of the loans. These principal payments are then passed through to bondholders, reducing the outstanding bond balance.

Accounting professionals must track:

Original bond balance per CUSIP

Principal payments received

Remaining bond balance

Interest payments made

Amortization schedules

Each reporting period, accounting records must be updated to reflect the new bond balances. This ensures that financial statements accurately reflect outstanding liabilities and interest expenses.

Bond amortization schedules are particularly important in securitization cusip bond accounting because different tranches may amortize at different speeds depending on payment priority and prepayment rates. Senior tranches may be paid down faster, while subordinate tranches may receive principal payments later in the life of the securitization.

Reporting, Reconciliation, and Compliance Requirements

Financial reporting and reconciliation are critical components of securitization cusip bond accounting. Institutions must prepare periodic reports showing bond balances, interest payments, principal distributions, and remaining loan pool balances. These reports are used by investors, auditors, regulators, and management.

Reconciliation involves matching:

Loan pool balances

Servicer reports

Investor distribution reports

Bond balances per CUSIP

Interest income and expense records

If discrepancies are found, accounting teams must investigate and correct them. Regular reconciliation ensures that accounting records match actual cash flows and investor payments.

Compliance is another important aspect of securitization cusip bond accounting. Financial institutions must comply with accounting standards such as GAAP or IFRS, as well as regulatory reporting requirements. Proper documentation, audit trails, and CUSIP-level tracking help ensure compliance and transparency.

Role of Audits and Forensic Accounting in CUSIP Bond Accounting

Audits and forensic reviews often focus heavily on securitization cusip bond accounting because securitization structures are complex and involve multiple parties. Auditors review accounting records to ensure that loans were properly transferred, bonds were properly issued, and cash flows were distributed correctly.

Forensic accountants may trace loans from origination through securitization using CUSIP numbers to verify ownership and transfer history. They may also review accounting records to ensure that investors received correct payments and that financial statements were reported accurately.

This makes securitization cusip bond accounting not only an accounting function but also an important part of financial transparency, audit verification, and risk management.

Importance of Accurate Securitization CUSIP Bond Accounting for Financial Professionals

For financial professionals, accurate securitization cusip bond accounting is essential for financial reporting, compliance, investor reporting, and audit preparation. Errors in accounting can lead to financial misstatements, regulatory penalties, and investor disputes.

Proper accounting ensures:

Accurate financial statements

Proper investor reporting

Regulatory compliance

Accurate bond balance tracking

Transparent cash flow reporting

Successful audits and forensic reviews

As securitization markets continue to grow, financial professionals must develop strong knowledge of securitization cusip bond accounting procedures, reporting requirements, and reconciliation processes. Understanding the full accounting lifecycle from loan securitization to bond payoff is essential for accountants, auditors, financial analysts, and structured finance professionals working in securitization and bond accounting environments.

Conclusion

In the world of structured finance and loan securitization, securitization cusip bond accounting plays a critical role in ensuring accurate financial reporting, transparency, and compliance. From the initial transfer of loan pools into securitization trusts to the issuance of bonds with unique CUSIP identifiers, every step requires precise accounting, tracking, and reconciliation. Financial professionals must carefully record bond issuance, interest income, principal payments, amortization schedules, and investor distributions at the CUSIP level to maintain accurate financial records and reporting.

Proper securitization cusip bond accounting also supports regulatory compliance, audit readiness, and investor reporting accuracy. Since securitized bonds often involve multiple tranches with different payment priorities and interest structures, accounting professionals must maintain detailed records and perform regular reconciliations between loan pools, servicer reports, and bond balances. Without proper accounting procedures, discrepancies can arise, leading to reporting errors and compliance risks.

Ultimately, securitization cusip bond accounting is not just an accounting function but a financial tracking and reporting system that ensures transparency throughout the life of securitized bonds. For financial professionals, auditors, and structured finance specialists, mastering securitization cusip bond accounting is essential for accurate reporting, risk management, and maintaining investor confidence in securitized financial instruments.

Build Stronger Cases with Expert Securitization & Forensic Audits

In today’s complex financial and securitization landscape, having accurate data, detailed audit reports, and reliable forensic analysis can make the difference between a weak case and a powerful one. That’s where our expertise makes an impact.

For over four years, we have been helping our associates build stronger, more defensible cases through professional securitization analysis and forensic audits. Our team specializes exclusively in business-to-business services, providing detailed CUSIP research, securitization reviews, bond analysis, and forensic reporting designed to support litigation, compliance, and financial investigations.

We understand that every case requires precision, documentation, and credible reporting. Our goal is to provide clear, accurate, and well-documented audit results that professionals can rely on with confidence. When you work with us, you gain a dedicated partner focused on delivering high-quality securitization and forensic audit support tailored to your business needs.

If you are looking to strengthen your cases with professional securitization and forensic audit services, we are here to help.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”