In modern structured finance and capital markets, accurate tracking, reporting, and management of bonds and asset-backed securities are critical for financial institutions, investors, auditors, and compliance professionals. One of the most important systems used to identify and track securities is the CUSIP identification system, which plays a central role in securitization and bond accounting. Understanding securitization cusip bond accounting is essential for anyone involved in mortgage-backed securities, asset-backed securities, collateralized debt obligations, and other structured financial products.

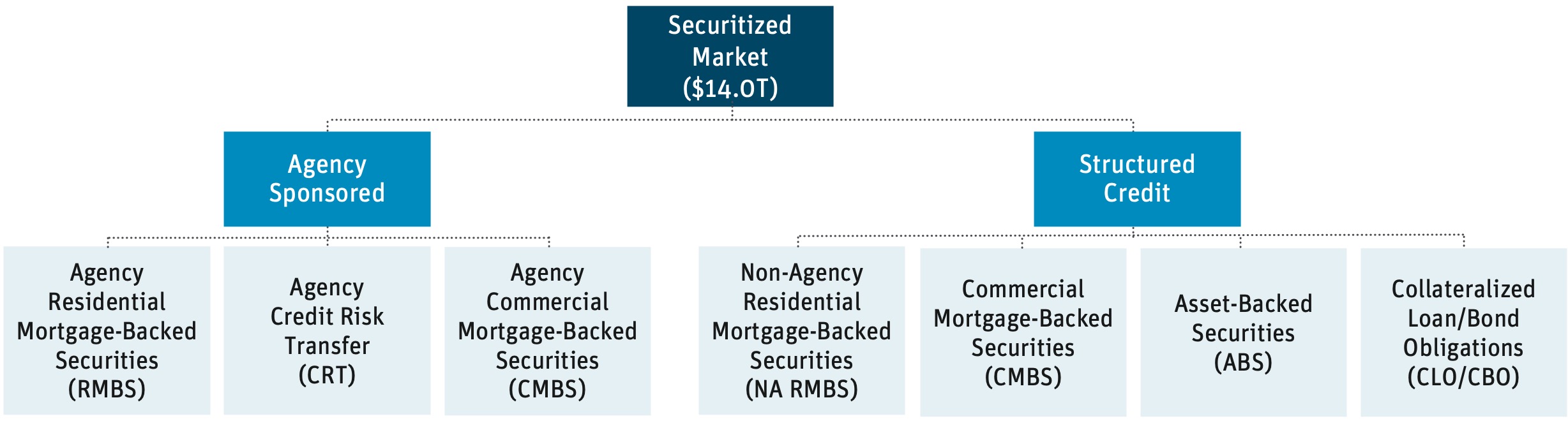

Securitization is the process of pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into tradable securities. These securities are then sold to investors in the form of bonds. Each bond or tranche issued in a securitization structure is assigned a unique CUSIP number, which allows financial institutions to track ownership, payments, interest reporting, and regulatory compliance. This is where securitization cusip bond accounting becomes a specialized area of financial reporting and structured finance management.

The CUSIP (Committee on Uniform Securities Identification Procedures) number is a nine-character alphanumeric code that uniquely identifies a financial instrument in the United States and Canada. In securitization transactions, multiple tranches of bonds are issued, and each tranche receives its own CUSIP. These tranches may have different interest rates, maturity dates, payment priorities, and risk levels. Proper accounting and reporting for each CUSIP is essential to ensure accurate financial statements, investor reporting, and compliance with accounting standards such as GAAP and IFRS.

Securitization cusip bond accounting involves tracking each bond tranche by its CUSIP, recording interest income, principal payments, amortization, and fair value adjustments. Financial institutions must maintain detailed records for each CUSIP because payments from the underlying asset pool are distributed to investors based on tranche priority, often referred to as the waterfall structure. Accounting professionals must ensure that all transactions related to each CUSIP are recorded correctly in the general ledger and reporting systems.

Structured finance transactions often involve trustees, servicers, custodians, and investment managers, all of whom rely on CUSIP numbers to track securities and cash flows. For example, when mortgage payments are collected from borrowers, the cash is distributed to different bond tranches identified by their CUSIP numbers. Accurate securitization cusip bond accounting ensures that interest and principal payments are allocated correctly and that investors receive accurate statements and tax reporting documents.

Another important aspect of securitization cusip bond accounting is compliance and reporting. Financial institutions must report holdings, valuations, and income associated with each CUSIP to regulators, investors, and auditors. This includes mark-to-market valuations, impairment analysis, and disclosure reporting. Without proper CUSIP-level accounting, it would be extremely difficult to track individual securities within large securitization pools that may contain hundreds of bond tranches.

Technology systems and structured finance accounting platforms are often used to manage securitization portfolios and CUSIP-level reporting. These systems track bond balances, interest accruals, payment histories, and amortization schedules for each CUSIP. Accounting teams rely on these systems to generate reports such as investor statements, portfolio valuations, and compliance reports. Proper system integration is a key component of effective securitization cusip bond accounting and structured finance management.

In addition, auditors and forensic analysts often review securitization transactions by examining CUSIP-level data to verify bond ownership, payment histories, and cash flow distributions. This is particularly important in mortgage-backed securities and asset-backed securities where multiple parties are involved in servicing, administration, and investment management. Accurate records maintained through securitization cusip bond accounting help ensure transparency, accountability, and financial accuracy in complex structured finance transactions.

Overall, securitization cusip bond accounting is a specialized accounting and financial management process that combines structured finance, bond accounting, security identification systems, and regulatory reporting. It plays a critical role in tracking securitized bonds, managing investor payments, ensuring financial reporting accuracy, and maintaining compliance with financial regulations. As structured finance markets continue to grow, the importance of accurate CUSIP-level bond accounting and reporting will continue to increase for financial institutions, auditors, investors, and compliance professionals involved in securitization and bond portfolio management.

Role of CUSIP Numbers in Securitization Bond Tracking

In structured finance transactions, the CUSIP number serves as the primary identifier for each bond tranche issued in a securitization deal. When loans such as mortgages, auto loans, or credit card receivables are pooled together and converted into securities, multiple bond tranches are created with different risk levels, maturity dates, and interest rates. Each of these tranches is assigned a unique CUSIP number so they can be tracked individually in financial systems. This is where securitization cusip bond accounting becomes essential for accurate financial management and reporting.

Financial institutions use CUSIP numbers to record bond purchases, sales, interest income, and principal repayments. Instead of tracking bonds only by deal name or issuer, accounting systems track each security at the CUSIP level. This allows accountants and portfolio managers to monitor performance, valuation, and cash flow for each specific tranche. Without CUSIP-level tracking, managing structured finance portfolios would be extremely difficult due to the large number of securities involved in securitization transactions.

CUSIP tracking also helps in reconciliation and reporting. Trustees, custodians, and servicers all use CUSIP numbers when reporting bond balances and payments. Accounting teams must reconcile their records with trustee reports using CUSIP numbers to ensure that balances, interest payments, and principal distributions match. Therefore, securitization cusip bond accounting plays a major role in reconciliation processes and financial accuracy.

Accounting Treatment for Securitized Bonds by CUSIP

Accounting for securitized bonds involves recording the purchase price, interest income, premium or discount amortization, and principal payments for each bond tranche identified by its CUSIP. When a financial institution purchases a securitized bond, the investment is recorded in the accounting system using the specific CUSIP associated with that bond. Over time, interest income is recorded based on the bond’s coupon rate, and principal payments reduce the bond’s carrying value.

If a bond is purchased at a premium or discount, the premium or discount must be amortized over the life of the bond using the effective interest method. This amortization must be tracked separately for each CUSIP because each tranche may have a different purchase price, yield, and maturity date. Proper securitization cusip bond accounting ensures that income recognition and bond valuation are accurate for financial reporting purposes.

Another important accounting treatment involves fair value adjustments. Many securitized bonds are classified as available-for-sale or trading securities, which means they must be reported at fair value on the balance sheet. Changes in fair value must be recorded periodically, and these adjustments are tracked at the CUSIP level. This allows financial institutions to monitor unrealized gains and losses for each individual security.

Cash Flow Allocation and Waterfall Structures

One of the most important aspects of securitization is the cash flow waterfall. In securitization transactions, cash flows from the underlying asset pool are distributed to bondholders based on a priority structure. Senior tranches receive payments first, followed by mezzanine tranches and then equity or residual tranches. Each tranche is identified by its CUSIP, and payments are allocated accordingly.

Accounting teams must record interest and principal payments received for each CUSIP separately. Since each tranche receives different payment amounts and at different times, securitization cusip bond accounting ensures that cash flow allocations are recorded correctly. This is particularly important for mortgage-backed securities where principal payments may vary due to prepayments and loan refinancing.

Waterfall reporting provided by trustees typically lists all payments by CUSIP number. Accounting teams use these reports to record journal entries for interest income, principal reductions, and realized gains or losses. Proper accounting ensures that financial statements accurately reflect investment income and bond balances.

Investor Reporting and Financial Statements

Investor reporting is another major area where securitization cusip bond accounting is used. Investment firms, banks, and asset managers must provide detailed reports showing bond holdings, income earned, market values, and portfolio performance. These reports are typically generated using CUSIP-level data so investors can see exactly which securities are held in a portfolio.

Financial statements also rely on CUSIP-level accounting data. Balance sheets show the total value of securitized bond investments, while income statements show interest income and realized gains or losses. Supporting schedules often list investments by CUSIP, including cost basis, market value, coupon rate, and maturity date. This level of detail is required for audits, regulatory reporting, and investor transparency.

Auditors frequently test investment balances by selecting specific CUSIPs and verifying purchase records, pricing data, and payment histories. Accurate securitization cusip bond accounting ensures that audit processes run smoothly and that financial records are properly documented.

Compliance and Regulatory Reporting Requirements

Financial institutions that invest in securitized bonds must comply with various regulatory reporting requirements. Regulators often require institutions to report investment holdings, risk exposure, and valuation data at the CUSIP level. This allows regulators to monitor exposure to mortgage-backed securities, asset-backed securities, and other structured finance instruments.

For example, banks may be required to report their investment portfolios in regulatory filings that include CUSIP numbers, book value, and fair value. Insurance companies and investment funds also provide similar reports to regulators and investors. Proper securitization cusip bond accounting ensures that these reports are accurate and compliant with regulatory standards.

Compliance also involves tracking credit ratings, maturity dates, and impairment indicators for each bond. If a securitized bond experiences credit deterioration, an impairment analysis must be performed and recorded in the accounting system. This analysis is done at the CUSIP level because each tranche may have different credit risk exposure.

Technology Systems Used in CUSIP Bond Accounting

Modern financial institutions rely heavily on technology systems to manage securitization portfolios and bond accounting. Investment accounting systems track securities by CUSIP and automate many accounting processes such as interest accruals, amortization, pricing updates, and reporting. These systems are essential for managing large portfolios containing hundreds or thousands of securitized bonds.

Portfolio management systems, trustee reporting systems, and accounting systems must be integrated to ensure accurate data flow. When trustee reports are received, accounting teams upload the data into their systems and reconcile balances by CUSIP. Automated systems reduce errors and improve efficiency in securitization cusip bond accounting.

Many institutions also use data providers to obtain market prices for securitized bonds. These prices are matched to securities using CUSIP numbers, allowing institutions to update fair values and calculate unrealized gains and losses. Without CUSIP identifiers, pricing and valuation processes would be much more complicated.

Reconciliation and Audit Procedures

Reconciliation is a critical part of securitization bond accounting. Accounting records must be reconciled with trustee statements, custodian reports, and portfolio statements to ensure accuracy. These reconciliations are typically performed using CUSIP numbers to match securities and balances across different reports.

Audit procedures also rely heavily on CUSIP-level data. Auditors may request documentation for specific securities identified by CUSIP, including purchase confirmations, pricing reports, and payment histories. Accurate securitization cusip bond accounting ensures that all documentation is organized and easily accessible for audit reviews.

Forensic accounting and securitization audits also involve reviewing CUSIP-level data to trace cash flows and verify bond ownership. This is particularly important in legal and financial investigations involving mortgage-backed securities and structured finance transactions.

Importance of Accurate Securitization CUSIP Bond Accounting in Structured Finance

Accurate securitization cusip bond accounting is essential for structured finance because it ensures proper tracking of investments, accurate income recognition, correct valuation, and compliance with financial reporting requirements. Structured finance transactions are complex and involve multiple parties, including issuers, trustees, servicers, investors, and regulators. CUSIP-level accounting provides a standardized way to track securities and financial transactions across all parties involved.

Errors in CUSIP bond accounting can lead to incorrect financial statements, reporting errors, compliance issues, and audit findings. Therefore, financial institutions invest significant resources in accounting systems, reconciliation processes, and internal controls to ensure accuracy in securitization bond accounting.

As structured finance markets continue to grow and become more complex, the importance of securitization cusip bond accounting will continue to increase. Financial professionals working in structured finance, investment accounting, auditing, and compliance must understand how CUSIP-based bond accounting works and how it supports financial reporting, investor reporting, and regulatory compliance.

Overall, securitization bond accounting using CUSIP numbers forms the foundation of structured finance investment tracking, reporting, and financial management. It allows institutions to manage complex bond portfolios, track cash flows accurately, produce financial reports, and maintain compliance with accounting and regulatory standards.

Conclusion

In the world of structured finance and investment management, securitization cusip bond accounting plays a critical role in ensuring accurate tracking, reporting, and management of securitized bonds and structured financial instruments. Since securitization transactions involve multiple bond tranches, payment structures, and investors, the use of CUSIP numbers allows financial institutions to identify, track, and manage each bond security individually. This makes accounting, reconciliation, reporting, and compliance much more efficient and accurate.

Proper securitization cusip bond accounting helps organizations record interest income, principal payments, premium and discount amortization, and fair value adjustments at the individual bond level. It also supports investor reporting, regulatory filings, audit reviews, and portfolio management. Without CUSIP-level accounting, managing complex securitization portfolios would be extremely difficult and prone to reporting errors.

As structured finance markets continue to expand, the importance of securitization cusip bond accounting will continue to grow for financial institutions, auditors, investors, and compliance professionals. Accurate accounting at the CUSIP level ensures transparency, financial accuracy, regulatory compliance, and proper bond portfolio management, making it a fundamental component of modern securitization and structured finance operations.

Build Stronger Cases with Expert Securitization and Forensic Audit Support

For over four years, we have been dedicated to helping our associates build stronger, more effective cases through detailed securitization analysis and forensic audits. Our experience, accuracy, and commitment to professional support have made us a trusted partner for businesses that require reliable securitization research, CUSIP analysis, and forensic loan audit services.

As an exclusively business-to-business provider, we understand the level of precision, documentation, and reporting that professionals need when working on complex financial, legal, and mortgage-related cases. Our team focuses on delivering clear, well-researched, and professionally prepared audit reports that help support case strategy, financial investigation, and structured finance analysis.

Whether you are working on mortgage securitization research, CUSIP tracing, loan ownership analysis, or forensic audit reporting, we are here to support your business with reliable and professional services tailored to your needs.

Contact us today to strengthen your case with professional securitization and forensic audit support.

📍 Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”