In the modern financial world, structured finance and asset-backed securities have become essential tools for banks, financial institutions, and investment firms. One of the most important yet often misunderstood areas within structured finance is securitization cusip bond accounting. This specialized accounting process involves tracking, recording, valuing, and reporting bonds that are created through securitization and identified using CUSIP numbers. Understanding this topic is crucial for accountants, auditors, financial analysts, and legal professionals working with mortgage-backed securities, asset-backed securities, and structured investment products.

Securitization cusip bond accounting refers to the accounting treatment and financial reporting of securitized bonds that are assigned unique CUSIP identifiers for tracking and trading purposes. When loans such as mortgages, auto loans, or credit card receivables are pooled together and converted into tradable securities, each security is assigned a CUSIP (Committee on Uniform Securities Identification Procedures) number. This number acts like a financial fingerprint, allowing institutions to track ownership, transactions, interest income, and valuation changes associated with the bond.

The accounting for these securities is not as simple as traditional bond accounting. In securitization, the original loans are transferred into a trust or special purpose vehicle (SPV), which then issues bonds to investors. These bonds generate income from the underlying loan payments. Therefore, securitization cusip bond accounting must address multiple components including asset transfer, bond issuance, interest income recognition, principal payments, fair value adjustments, and investor reporting. Each of these components requires specific journal entries and proper classification in financial statements.

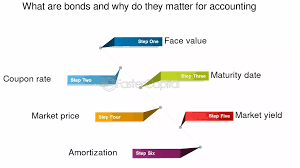

Another important aspect of securitization cusip bond accounting is valuation. Securitized bonds are often classified as held-to-maturity, available-for-sale, or trading securities depending on the intent of the investor. The valuation method may involve amortized cost, fair market value, or mark-to-market accounting. Changes in valuation must be properly recorded in financial statements, either through profit and loss statements or other comprehensive income, depending on accounting standards such as GAAP or IFRS.

Financial reporting is also a major component of securitization cusip bond accounting. Institutions must maintain detailed records for each CUSIP bond, including purchase price, interest income, principal repayments, amortization of premium or discount, and market value changes. These records are necessary for audits, compliance, investor reporting, and regulatory filings. Proper reporting ensures transparency and helps investors and regulators understand the performance and risk associated with securitized bonds.

In addition, forensic accounting and securitization audits often rely heavily on securitization cusip bond accounting records to trace loan ownership, cash flows, and bond performance. This is particularly important in mortgage securitization cases, where auditors and legal professionals analyze loan transfers and securitization structures using CUSIP numbers to identify specific securities and transactions.

Overall, securitization cusip bond accounting is a specialized accounting field that combines elements of bond accounting, structured finance, investment accounting, and financial reporting. It requires a strong understanding of securitization structures, journal entries, valuation methods, and reporting standards. As securitized securities continue to play a major role in global financial markets, the importance of accurate accounting and reporting for these instruments continues to grow. Understanding the fundamentals of this accounting process is essential for anyone involved in structured finance, auditing, investment analysis, or financial reporting related to securitized bonds.

Top of Form

Understanding the Structure Behind Securitized Bonds

To fully understand securitization cusip bond accounting, it is important to first understand how securitization works. Securitization is the process of pooling financial assets such as mortgages, auto loans, student loans, or credit card receivables and converting them into tradable securities. These securities are then sold to investors in the form of bonds. Each bond issued from the securitization pool is assigned a unique CUSIP number so it can be tracked in financial markets, accounting systems, and reporting platforms.

In a typical securitization transaction, the originator transfers loans to a Special Purpose Vehicle (SPV) or trust. The trust then issues bonds to investors, and the cash flow from the underlying loans is used to pay interest and principal to bondholders. From an accounting perspective, this is where securitization cusip bond accounting becomes essential because each bond must be recorded, tracked, valued, and reported separately using its CUSIP identifier.

The accounting becomes more complex because the transaction involves asset transfers, bond issuance, servicing fees, interest income distribution, and principal repayments. Proper accounting ensures that all financial records accurately reflect the movement of assets and liabilities associated with the securitization structure.

Journal Entries in Securitization CUSIP Bond Accounting

Journal entries are one of the most important components of securitization cusip bond accounting. These entries record the purchase of securitized bonds, interest income, principal repayments, and valuation adjustments.

When an investor purchases a securitized bond, the initial journal entry typically records the investment in securities and the cash paid for the bond. If the bond is purchased at a premium or discount, the difference must be amortized over the life of the bond.

Interest income is recorded periodically as payments are received from the securitization trust. The interest portion is recorded as income, while the principal portion reduces the carrying value of the investment. This is a critical part of securitization cusip bond accounting because securitized bonds often have structured cash flows where each payment includes both principal and interest components.

If the bond is classified as available-for-sale or trading, market value adjustments must be recorded periodically. These adjustments ensure that the bond is reflected at fair value in financial statements.

Proper journal entries help maintain accurate financial records and ensure compliance with accounting standards such as GAAP and IFRS. Without accurate journal entries, financial reporting related to securitized bonds can become misleading or incorrect.

Valuation Methods for Securitized Bonds

Valuation is another major area in securitization cusip bond accounting. Securitized bonds are not always valued at their purchase price. Instead, they may be valued based on amortized cost or fair market value depending on how the investment is classified.

If the bond is classified as Held-to-Maturity, it is usually recorded at amortized cost. This means the premium or discount is amortized over the life of the bond, and the bond is not adjusted to market value regularly.

If the bond is classified as Available-for-Sale, it must be marked to market, and unrealized gains or losses are recorded in Other Comprehensive Income.

If the bond is classified as Trading Securities, unrealized gains and losses are recorded directly in the income statement.

Valuation becomes more complicated in securitization cusip bond accounting because securitized bonds are often influenced by interest rates, prepayment speeds, default rates, and credit risk of the underlying loans. Therefore, valuation models often include discounted cash flow analysis, yield analysis, and market pricing models.

Accurate valuation is important because it affects financial statements, investor reporting, and regulatory compliance. Incorrect valuation can lead to misstated financial statements and compliance issues.

Reporting Requirements and Financial Statements

Financial reporting is a critical component of securitization cusip bond accounting. Companies and financial institutions must report their securitized bond holdings in their financial statements, including balance sheets, income statements, and disclosures.

On the balance sheet, securitized bonds are recorded as investments in securities. The value reported depends on the classification of the security. Interest income from securitized bonds is reported on the income statement, while unrealized gains and losses may be reported either in income or equity depending on classification.

In addition to financial statements, institutions must maintain detailed CUSIP-level reports. These reports typically include purchase date, purchase price, interest rate, principal balance, market value, and income earned. These reports are essential for audits, investor reporting, and compliance reviews.

This is why securitization cusip bond accounting requires strong documentation and tracking systems. Each CUSIP bond must be tracked individually to ensure accurate reporting and compliance with financial regulations.

Amortization of Premium and Discount

Another important concept in securitization cusip bond accounting is the amortization of bond premium or discount. When a bond is purchased above its face value, the difference is called a premium. When purchased below face value, the difference is called a discount.

This premium or discount must be amortized over the life of the bond using methods such as the effective interest method. The amortization affects interest income and the carrying value of the bond on the balance sheet.

For securitized bonds, amortization schedules can be more complex because principal payments may occur monthly due to loan repayments and prepayments. Therefore, accountants must update amortization schedules regularly to reflect changing principal balances.

This makes securitization cusip bond accounting more complex than traditional bond accounting because cash flows are not always fixed and predictable.

Role of CUSIP Numbers in Tracking and Accounting

CUSIP numbers play a central role in securitization cusip bond accounting because they uniquely identify each security. Financial institutions use CUSIP numbers to track bond purchases, sales, interest income, principal payments, and market value changes.

Accounting systems often track investments at the CUSIP level rather than at the portfolio level. This allows detailed reporting and auditing. Auditors often request CUSIP-level reports to verify investment balances, income, and valuation adjustments.

CUSIP tracking also helps in forensic audits and securitization reviews where analysts trace loan pools and bond issuances. By tracking securities using CUSIP numbers, accountants and auditors can verify ownership and cash flow distribution.

Without proper CUSIP tracking, securitization cusip bond accounting would be extremely difficult, especially for institutions holding large portfolios of securitized bonds.

Compliance, Audit, and Regulatory Considerations

Compliance and audit requirements are another major reason why securitization cusip bond accounting is important. Financial institutions must comply with accounting standards, regulatory reporting requirements, and audit standards.

Auditors typically review securitized bond investments to verify valuation, income recognition, and classification. They may also review CUSIP-level reports, amortization schedules, and fair value calculations.

Regulators may require detailed investment reporting, especially for banks, insurance companies, and investment firms. Proper accounting ensures that institutions remain compliant with financial regulations and reporting standards.

Failure to maintain proper securitization cusip bond accounting records can result in audit findings, compliance violations, and financial statement restatements.

Importance of Accurate Securitization CUSIP Bond Accounting

Accurate securitization cusip bond accounting is essential for financial transparency, investment tracking, income recognition, valuation, and regulatory compliance. Because securitized bonds involve complex cash flows, structured payments, and market value changes, proper accounting ensures that financial statements accurately reflect investment performance.

It also helps investors, auditors, and regulators understand the true value and performance of securitized bond investments. As securitization continues to be a major part of global financial markets, the importance of proper accounting, reporting, and valuation of securitized bonds will continue to grow.

Understanding journal entries, valuation methods, reporting requirements, amortization, and CUSIP tracking is essential for anyone involved in structured finance, investment accounting, securitization audits, or financial reporting. This is why securitization cusip bond accounting is considered a specialized and highly important area of accounting and financial reporting.

Conclusion

In conclusion, securitization cusip bond accounting is a specialized area of financial accounting that plays a critical role in tracking, valuing, and reporting securitized bond investments. Because securitized bonds are created from pools of financial assets and issued through structured finance transactions, their accounting treatment is more complex than traditional bond accounting. Each security is tracked using a unique CUSIP number, which allows accountants, auditors, and financial institutions to monitor interest income, principal repayments, amortization, and market value changes accurately.

Proper securitization cusip bond accounting involves recording journal entries for bond purchases, interest income recognition, premium or discount amortization, and fair value adjustments. It also includes detailed financial reporting, CUSIP-level tracking, and compliance with accounting standards such as GAAP or IFRS. Accurate valuation and reporting are essential because they directly affect financial statements, investment reporting, and regulatory compliance.

As securitization continues to be widely used in mortgage-backed securities, asset-backed securities, and structured finance markets, the importance of securitization cusip bond accounting will continue to grow. Organizations that maintain accurate accounting records, proper valuation methods, and detailed CUSIP tracking systems can ensure transparency, compliance, and better financial decision-making related to securitized bond investments.

Bottom of Form

Bottom of Form

Build Stronger Cases with Expert Securitization & Forensic Audits

When your case depends on accuracy, documentation, and financial truth, you need more than basic research—you need experts who understand securitization, CUSIP tracking, and forensic loan analysis at a professional level. For over four years, we have been helping our associates build stronger, more effective cases through detailed securitization and forensic audits designed specifically for legal, financial, and investigative professionals.

We are proud to be an exclusively business-to-business provider, working with attorneys, auditors, investigators, and financial professionals who require reliable, well-documented securitization reports and CUSIP research. Our work is designed to support litigation, case preparation, forensic analysis, and financial investigation with clear, accurate, and professional documentation.

Whether you need securitization chain analysis, CUSIP bond research, loan audit reports, or forensic accounting support, our team is committed to delivering accurate data, detailed reports, and dependable support that helps you build stronger and more defensible cases.

If your firm or organization needs professional securitization and forensic audit support, we are ready to work with you.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”