Introduction

In the complex world of structured finance, accurate identification, tracking, and reporting of securities are essential for transparency, compliance, and financial accuracy. One of the most critical components in this process is securitization cusip bond accounting, which plays a vital role in managing securitized instruments such as mortgage-backed securities (MBS), asset-backed securities (ABS), collateralized loan obligations (CLOs), and other structured financial products. Financial institutions, investment firms, accounting professionals, and compliance teams rely heavily on proper accounting practices tied to CUSIP identifiers to ensure accurate reporting, regulatory compliance, and portfolio management.

Securitization cusip bond accounting refers to the accounting and tracking process of bonds and securities that are created through securitization and identified using CUSIP numbers. A CUSIP (Committee on Uniform Securities Identification Procedures) number is a unique nine-character alphanumeric code assigned to financial instruments such as bonds, stocks, and securitized products. These identifiers help institutions track securities across trading, settlement, accounting, and reporting systems. Without proper CUSIP tracking, financial reporting can become inaccurate, compliance risks may increase, and reconciliation processes can become extremely difficult.

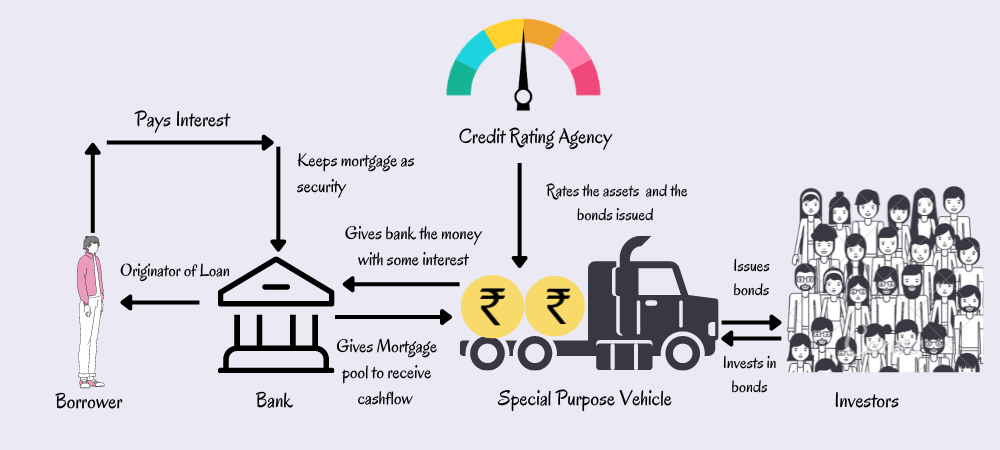

Securitization itself is the process of pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into tradable securities that investors can purchase. Each tranche of these securities is assigned a unique CUSIP number, which allows accountants and financial analysts to track interest income, principal payments, amortization, and valuation for each specific security. This is where securitization cusip bond accounting becomes essential, as each tranche may have different interest rates, maturity dates, risk levels, and payment structures.

From an accounting perspective, securitized bonds must be properly recorded on the balance sheet, income statement, and investment schedules. Accountants must track coupon payments, premium or discount amortization, fair value adjustments, and principal repayments associated with each CUSIP. In large investment portfolios where thousands of securities are held, securitization cusip bond accounting ensures that each security is properly recorded and reconciled with custodians, trustees, and portfolio management systems.

Another important aspect of securitization cusip bond accounting is compliance and regulatory reporting. Financial institutions must comply with accounting standards such as GAAP, IFRS, and regulatory frameworks set by authorities like the SEC, FINRA, and other financial regulators. Proper CUSIP-level accounting helps institutions generate accurate reports for audits, regulatory filings, and investor disclosures. Without accurate CUSIP-level tracking, institutions may face reporting errors, audit issues, or compliance penalties.

Technology also plays a major role in modern securitization cusip bond accounting. Many firms use specialized accounting software, portfolio management systems, and reconciliation platforms to automate CUSIP tracking, interest calculations, amortization schedules, and valuation updates. Automation reduces manual errors and improves efficiency in managing large securitized portfolios. However, even with automation, accounting teams must understand the underlying accounting principles, reporting requirements, and reconciliation processes associated with securitized bonds.

In today’s financial environment, where structured products and securitized instruments are widely used by banks, hedge funds, insurance companies, and asset managers, securitization cusip bond accounting has become an essential function in financial operations. It supports accurate investment accounting, financial reporting, compliance management, and portfolio analysis. Professionals working in investment accounting, structured finance, fund accounting, and financial reporting must understand how CUSIP-based accounting works in securitization structures.

This complete guide will explain how securitization cusip bond accounting works, how securities are tracked using CUSIP numbers, how accounting entries are recorded, how reporting and compliance requirements are handled, and what best practices organizations should follow to ensure accuracy and efficiency in securitized bond accounting.

Understanding the Basics of Securitization CUSIP Bond Accounting

Securitization cusip bond accounting begins with understanding how securitized bonds are created and identified. In securitization, financial assets such as mortgages, auto loans, credit card receivables, or student loans are pooled together and converted into securities that investors can purchase. These securities are divided into tranches, and each tranche is assigned a unique CUSIP number. This unique identifier is essential for tracking each security separately for accounting, reporting, and compliance purposes.

In accounting systems, each CUSIP represents a specific investment instrument with its own interest rate, maturity date, payment schedule, and risk level. Because securitized instruments often involve thousands of individual securities, securitization cusip bond accounting helps organizations track each bond at the individual security level rather than at the portfolio level. This improves accuracy in financial reporting and investment tracking.

Accounting teams use CUSIP numbers to record purchase transactions, interest income, amortization, principal payments, and fair value adjustments. Without CUSIP-level tracking, it would be extremely difficult to reconcile investment records with custodian statements and trustee reports.

Role of CUSIP Numbers in Bond Tracking and Identification

CUSIP numbers are the foundation of securitization cusip bond accounting because they act as unique identifiers for each bond or tranche in a securitized structure. Every transaction related to a bond — including purchase, sale, interest payment, principal repayment, or valuation adjustment — is recorded using the CUSIP number.

When investment firms purchase securitized bonds, the accounting system records the investment using the CUSIP identifier. Interest payments received are matched to the correct CUSIP, ensuring that income is recorded accurately. Similarly, principal repayments and amortization entries are recorded against the specific CUSIP.

This level of tracking is especially important in mortgage-backed securities and asset-backed securities where cash flows are complex and vary by tranche. Securitization cusip bond accounting ensures that each tranche is accounted for separately and accurately.

CUSIP tracking also helps in reconciliation with custodians, trustees, and portfolio management systems. Since all financial institutions use CUSIP numbers as standard identifiers, reconciliation becomes easier and more accurate.

Accounting Entries in Securitization CUSIP Bond Accounting

One of the most important aspects of securitization cusip bond accounting is recording accounting entries related to bond transactions and cash flows. These entries typically include bond purchases, interest income, premium or discount amortization, principal repayments, and fair value adjustments.

When a securitized bond is purchased, the investment is recorded at cost. If the bond is purchased at a premium or discount, the difference between the purchase price and par value must be amortized over the life of the bond. This amortization is recorded periodically and linked to the specific CUSIP.

Interest income is recorded when coupon payments are received or accrued. Since each tranche may have a different interest rate, securitization cusip bond accounting ensures that interest income is calculated and recorded correctly for each individual security.

Principal repayments are also recorded at the CUSIP level. In many securitized products, principal is paid periodically rather than at maturity. Accounting systems must track these principal payments and reduce the bond’s carrying value accordingly.

Fair value adjustments are recorded if the bonds are classified as available-for-sale or trading securities. These valuation adjustments are also tracked at the CUSIP level to ensure accurate financial reporting.

Reporting Requirements and Financial Statements

Financial reporting is a major component of securitization cusip bond accounting. Investment portfolios containing securitized bonds must be reported accurately in financial statements, investment schedules, and regulatory filings.

Accounting teams must prepare reports showing investment balances, interest income, realized gains or losses, unrealized gains or losses, and amortized cost for each CUSIP. These reports are used for financial statements, investor reporting, and regulatory compliance.

CUSIP-level reporting allows organizations to generate detailed investment reports, including:

- Investment holdings reports

- Interest income reports

- Amortization schedules

- Realized gain/loss reports

- Fair value reports

- Portfolio valuation reports

Without securitization cusip bond accounting, generating these reports would be extremely difficult and prone to errors.

CUSIP-level reporting also helps auditors verify investment balances and income recorded in the financial statements. Auditors often request investment reports sorted by CUSIP to verify existence, valuation, and income recognition.

Compliance and Regulatory Considerations

Compliance is another critical area where securitization cusip bond accounting plays an important role. Financial institutions must comply with accounting standards such as GAAP or IFRS, as well as regulatory requirements from financial authorities.

Regulators often require detailed reporting of investment holdings, especially for structured products and securitized instruments. These reports must include CUSIP numbers, security descriptions, maturity dates, interest rates, and valuation information.

Proper securitization cusip bond accounting ensures that institutions can meet regulatory reporting requirements and avoid compliance issues. It also helps during audits and regulatory examinations, where institutions must provide detailed investment records.

Failure to maintain accurate CUSIP-level accounting records can lead to reporting errors, audit findings, compliance penalties, and reputational risks.

Technology and Automation in Securitization CUSIP Bond Accounting

Modern financial institutions rely heavily on technology to manage securitization cusip bond accounting. Investment accounting systems, portfolio management systems, and reconciliation platforms automate many accounting processes related to securitized bonds.

These systems can automatically import CUSIP data, interest rates, payment schedules, and market prices. They can also automatically calculate interest income, amortization, and fair value adjustments. Automation reduces manual errors and improves efficiency in accounting operations.

Reconciliation systems also use CUSIP numbers to match internal accounting records with custodian statements and trustee reports. This ensures that investment balances and transactions are accurate and complete.

Technology has made securitization cusip bond accounting more efficient, but accounting professionals still need to understand the accounting principles and reporting requirements behind the automation.

Reconciliation and Portfolio Management

Reconciliation is an essential part of securitization cusip bond accounting. Accounting records must be reconciled with custodian statements, trustee reports, and portfolio management systems to ensure accuracy.

Reconciliation is typically performed at the CUSIP level, where accounting teams compare investment balances, interest income, and principal payments recorded in the accounting system with external statements.

Any differences must be investigated and corrected. These differences may be caused by timing differences, incorrect interest calculations, missing transactions, or valuation differences.

Proper reconciliation ensures that financial statements are accurate and that investment records are complete. Securitization cusip bond accounting makes reconciliation easier because all transactions are tracked using standardized CUSIP identifiers.

Portfolio managers also use CUSIP-level data to analyze investment performance, interest income, cash flows, and portfolio risk. Accurate accounting data supports better investment decision-making and portfolio management.

Best Practices for Securitization CUSIP Bond Accounting

Organizations should follow best practices to ensure effective securitization cusip bond accounting. One important best practice is maintaining accurate security master data for each CUSIP, including interest rate, maturity date, payment frequency, and security type.

Another best practice is performing regular reconciliations with custodians and trustees to ensure that investment balances and income records are accurate. Regular reconciliation helps identify errors early and prevents reporting issues.

Automation should also be used wherever possible to reduce manual data entry and calculation errors. Investment accounting systems can automate interest calculations, amortization, and valuation updates.

Documentation is also important in securitization cusip bond accounting. Organizations should maintain proper documentation for investment transactions, accounting policies, and reconciliation procedures. This documentation is useful during audits and regulatory examinations.

Training accounting staff on securitized products and CUSIP-based accounting is also important. Structured finance instruments can be complex, and accounting teams must understand how cash flows, amortization, and valuations work.

Importance of Accuracy in Securitization CUSIP Bond Accounting

Accuracy is extremely important in securitization cusip bond accounting because investment balances, interest income, and valuations directly impact financial statements and investor reports. Errors in accounting can lead to incorrect financial reporting, audit issues, and compliance problems.

Accurate CUSIP-level accounting ensures that each security is properly tracked, income is recorded correctly, and valuations are accurate. This improves financial transparency and investor confidence.

As securitized products continue to grow in financial markets, the importance of securitization cusip bond accounting will continue to increase. Financial institutions must maintain strong accounting systems, reconciliation processes, and reporting procedures to manage securitized bond portfolios effectively and remain compliant with accounting and regulatory requirements.

Conclusion

In today’s complex financial environment, securitization cusip bond accounting plays a critical role in ensuring accurate tracking, reporting, and compliance for securitized instruments such as mortgage-backed securities, asset-backed securities, and other structured finance products. Because each securitized bond tranche carries unique characteristics such as interest rates, maturity dates, and payment structures, CUSIP-level accounting becomes essential for maintaining accurate financial records and investment reporting.

Proper securitization cusip bond accounting helps organizations record interest income, amortization, principal repayments, and fair value adjustments accurately for each individual security. This level of detailed tracking not only improves financial reporting accuracy but also supports regulatory compliance, audit requirements, and portfolio management decisions. Financial institutions, asset managers, insurance companies, and investment firms rely heavily on CUSIP-based accounting systems to manage large investment portfolios efficiently.

Additionally, automation and modern investment accounting systems have made securitization cusip bond accounting more efficient and reliable, reducing manual errors and improving reconciliation processes with custodians and trustees. However, strong accounting knowledge, proper reconciliation procedures, and accurate reporting practices are still essential for success.

Overall, securitization cusip bond accounting is a fundamental component of structured finance operations, ensuring transparency, accuracy, compliance, and effective investment management in today’s securitized financial markets.

Build Stronger Cases with Expert Securitization & Forensic Audit Support

For over four years, Mortgage Audits Online has been a trusted partner for businesses seeking reliable, accurate, and professional securitization and forensic audit services. We specialize exclusively in business-to-business support, helping our associates build stronger, data-driven cases with detailed securitization analysis, CUSIP research, and forensic mortgage audits.

Our team understands the complexity of securitization, loan transfers, and structured finance documentation. That is why we focus on delivering clear, well-researched, and professionally prepared audit reports that help our partners strengthen their case strategies, improve documentation accuracy, and uncover critical securitization details.

When you work with Mortgage Audits Online, you are not just ordering a report — you are partnering with a team that is committed to accuracy, professionalism, confidentiality, and long-term business relationships. We take pride in supporting law firms, audit firms, consultants, and financial professionals with dependable securitization and forensic audit services.

If your organization needs reliable securitization research, CUSIP data analysis, or forensic mortgage audit support, we are here to help you every step of the way.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

Phone: 877-399-2995

Fax: 877-398-5288

Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”