Introduction

In the complex world of structured finance, securitization cusip bond accounting plays a critical role in ensuring accurate financial reporting, bond tracking, and regulatory compliance. As financial institutions continue to bundle loans into securities and sell them to investors, proper accounting and identification of these securities become essential for transparency and risk management. Without proper accounting practices, institutions may face reporting errors, compliance issues, and financial discrepancies that can impact investors, auditors, and regulatory authorities.

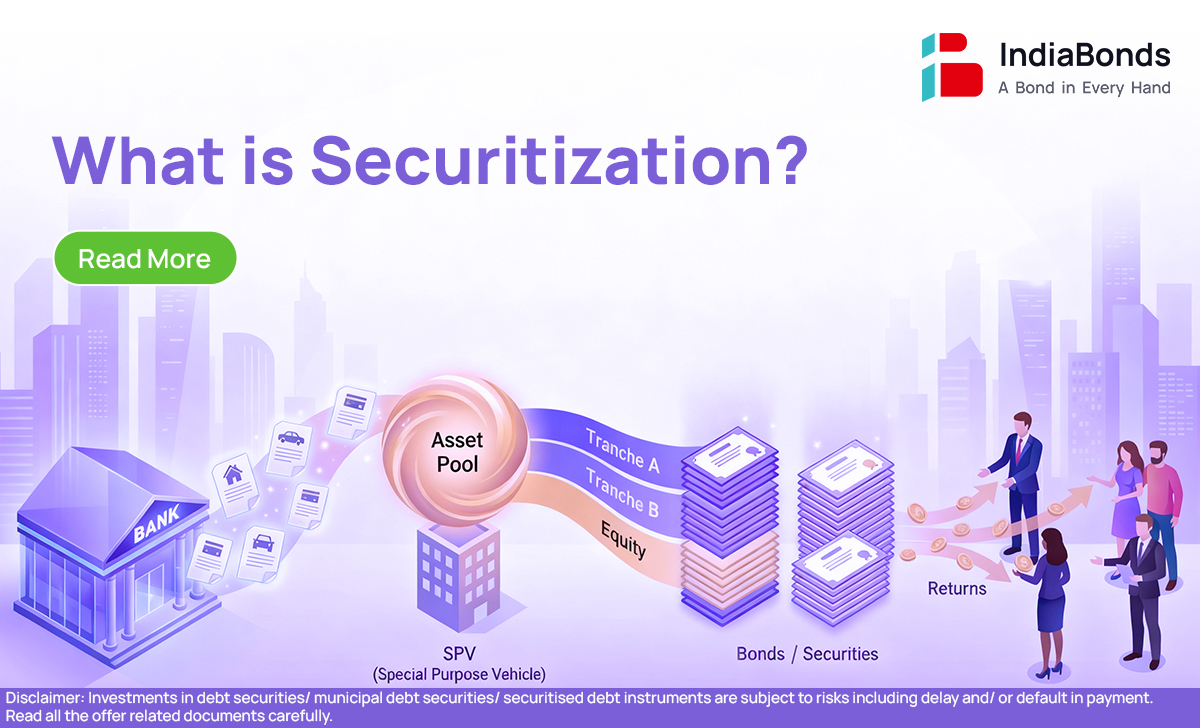

Securitization involves pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into tradable securities. Each of these securities is assigned a unique CUSIP number, which serves as an identifier for tracking and reporting purposes. This is where securitization cusip bond accounting becomes essential, as it allows financial professionals to monitor bond performance, interest payments, principal distributions, and ownership changes accurately. The CUSIP system ensures that each security can be tracked throughout its lifecycle, from issuance to maturity.

One of the main purposes of securitization cusip bond accounting is to maintain accurate financial records for mortgage-backed securities (MBS), asset-backed securities (ABS), and collateralized debt obligations (CDOs). These financial instruments often involve multiple tranches, each with different risk levels, interest rates, and payment structures. Proper accounting helps institutions track each tranche separately, ensuring that investors receive the correct payments and that financial statements reflect accurate asset valuations. Without proper tracking systems tied to CUSIP numbers, managing these complex securities would be extremely difficult.

Another important aspect of securitization cusip bond accounting is compliance with financial reporting standards and regulatory requirements. Financial institutions must follow accounting frameworks such as GAAP or IFRS when reporting securitized assets and bond holdings. Accurate accounting ensures that income recognition, impairment reporting, and asset valuation are handled correctly. Regulators and auditors often review CUSIP-level data to verify bond ownership, payment histories, and valuation accuracy, making detailed accounting records essential for compliance and audit readiness.

In addition to regulatory compliance, securitization cusip bond accounting helps improve transparency and risk management. Investors rely on accurate bond tracking and reporting to evaluate the performance of securitized assets. If accounting records are inaccurate or incomplete, investors may not be able to properly assess risk exposure, cash flow performance, or bond valuation. Accurate accounting allows institutions to monitor delinquencies, defaults, prepayments, and interest income associated with each CUSIP-identified security.

Technology has significantly improved securitization cusip bond accounting processes in recent years. Modern accounting systems and bond tracking software can automatically track securities using CUSIP numbers, generate reports, calculate interest accruals, and reconcile bond holdings with custodial records. Automation reduces manual errors, improves reporting efficiency, and ensures that financial institutions maintain accurate and up-to-date records of their securitized bond portfolios.

Furthermore, securitization cusip bond accounting is essential for portfolio management and financial analysis. Portfolio managers use CUSIP-level accounting data to track bond performance, calculate yields, analyze cash flows, and manage risk exposure. Accurate accounting data helps institutions make informed investment decisions and maintain balanced portfolios across different asset classes and risk categories.

As securitization markets continue to grow and financial instruments become more complex, the importance of securitization cusip bond accounting continues to increase. Accurate bond tracking, proper financial reporting, and regulatory compliance all depend on well-maintained accounting systems that track securities at the CUSIP level. Institutions that implement strong accounting practices and proper tracking systems can reduce risk, improve transparency, and ensure accurate financial reporting.

Understanding the fundamentals and best practices of securitization cusip bond accounting is therefore essential for accountants, financial analysts, auditors, and investment professionals who work with securitized assets and bond portfolios. Proper accounting not only ensures compliance and reporting accuracy but also supports better financial decision-making and portfolio management in the structured finance industry.

Importance of Accurate Bond Identification in Securitization

In the structured finance industry, accurate identification of bonds is essential for proper tracking, reporting, and compliance. This is where securitization cusip bond accounting becomes extremely important. Each securitized bond is assigned a unique CUSIP number that allows financial institutions, investors, and regulators to track specific securities throughout their lifecycle. Without proper identification, it would be difficult to distinguish between different bond tranches, payment structures, and maturity dates.

CUSIP numbers serve as the backbone of bond tracking systems. When accounting teams record transactions, interest payments, or principal reductions, they must assign them to the correct CUSIP. This ensures that financial records remain accurate and that investors receive correct payment allocations. Accurate identification also helps prevent accounting errors, duplicate reporting, and reconciliation issues.

Financial institutions often manage thousands of securitized bonds simultaneously, making proper identification systems essential. Securitization cusip bond accounting ensures that each bond is properly recorded, tracked, and reported in financial statements and investor reports.

Role of CUSIP Numbers in Bond Tracking and Reporting

CUSIP numbers play a central role in tracking bond ownership, payment history, and valuation. In securitization cusip bond accounting, every transaction related to a securitized bond is recorded under its specific CUSIP identifier. This includes bond purchases, sales, transfers, interest income, and principal repayments.

Bond tracking systems use CUSIP numbers to generate reports such as portfolio holdings reports, interest income reports, and valuation reports. These reports are essential for financial reporting, tax reporting, and investment analysis. Without accurate CUSIP-based accounting, financial institutions would struggle to maintain accurate bond portfolios.

Another important function of CUSIP tracking is reconciliation. Institutions must regularly reconcile their internal accounting records with custodial statements and trustee reports. Securitization cusip bond accounting helps ensure that bond balances, payments, and valuations match across all records and systems.

Accounting Treatment for Securitized Bonds

Accounting for securitized bonds involves recording interest income, principal payments, amortization, and fair value adjustments. Securitization cusip bond accounting ensures that each of these accounting entries is recorded correctly for each individual bond.

Interest income is typically recorded using the effective interest rate method, which spreads interest income over the life of the bond. Principal payments reduce the carrying value of the bond asset on the balance sheet. If the bond was purchased at a premium or discount, amortization must be recorded periodically to adjust the bond’s book value.

Fair value adjustments may also be required depending on accounting standards and whether the bond is classified as held-to-maturity, available-for-sale, or trading security. Proper accounting treatment ensures that financial statements accurately reflect the value and performance of securitized bond investments.

Reporting Requirements and Regulatory Compliance

Financial institutions must comply with strict reporting and regulatory requirements when dealing with securitized bonds. Securitization cusip bond accounting helps institutions meet these requirements by maintaining accurate records of bond holdings, income, and valuations.

Regulators often require detailed reporting at the CUSIP level to ensure transparency in financial markets. These reports may include bond holdings, payment histories, default rates, and valuation changes. Auditors also rely on CUSIP-level accounting records when reviewing financial statements and verifying asset balances.

Proper accounting and reporting reduce the risk of regulatory penalties, audit findings, and financial misstatements. Institutions that maintain accurate CUSIP-level records are better prepared for audits and regulatory reviews.

Cash Flow Tracking and Payment Allocation

One of the most important aspects of securitization cusip bond accounting is tracking cash flows associated with securitized bonds. These cash flows include interest payments, principal repayments, and prepayments.

Securitized bonds often have complex payment structures with multiple tranches receiving payments in different priority levels. Accounting systems must track how cash flows are allocated to each tranche and each CUSIP. This ensures that investors receive correct payments and that accounting records reflect accurate income and principal balances.

Cash flow tracking also helps financial institutions analyze bond performance, prepayment speeds, and default rates. Accurate cash flow accounting is essential for investment analysis and portfolio management.

Reconciliation and Error Prevention

Reconciliation is a critical part of securitization cusip bond accounting. Institutions must regularly reconcile their accounting records with trustee reports, custodian statements, and portfolio management systems.

Reconciliation helps identify discrepancies such as missing payments, incorrect balances, duplicate entries, or valuation differences. Early detection of errors prevents financial reporting issues and ensures that records remain accurate.

Automated reconciliation tools have become increasingly popular in securitized bond accounting. These tools match transactions and balances across multiple systems using CUSIP numbers, reducing manual work and minimizing errors.

Technology and Automation in Bond Accounting

Modern accounting systems have significantly improved securitization cusip bond accounting processes. Automation allows institutions to track bonds, record transactions, calculate interest income, and generate reports automatically.

Bond accounting software can integrate with trustee systems, custodial systems, and portfolio management platforms to provide real-time bond tracking and reporting. Automation reduces manual data entry, improves accuracy, and increases efficiency.

Technology also helps institutions generate detailed reports such as CUSIP-level income reports, valuation reports, and portfolio performance reports. These reports are essential for financial reporting, audits, and investment decision-making.

Portfolio Management and Investment Analysis

Portfolio managers rely heavily on securitization cusip bond accounting data to manage bond portfolios and analyze investment performance. CUSIP-level data allows portfolio managers to track individual bond performance, calculate yields, analyze cash flows, and monitor risk exposure.

Accurate accounting data helps portfolio managers make informed decisions about buying, selling, or holding securitized bonds. It also helps them diversify portfolios across different asset classes, maturities, and risk levels.

Investment analysis often involves reviewing historical performance, cash flow projections, and valuation trends for individual CUSIP securities. Without accurate accounting records, portfolio analysis would be unreliable.

Risk Management and Performance Monitoring

Risk management is another major reason why securitization cusip bond accounting is important. Financial institutions must monitor credit risk, interest rate risk, and prepayment risk associated with securitized bonds.

CUSIP-level accounting allows institutions to track bond performance and identify underperforming assets. If a particular bond shows increased defaults or reduced cash flows, risk managers can take action to reduce exposure.

Performance monitoring also helps institutions evaluate the profitability of securitized bond investments. Accurate accounting records provide detailed income, cash flow, and valuation data needed for performance analysis.

Best Practices for Accurate Bond Tracking and Reporting

There are several best practices that institutions should follow to improve securitization cusip bond accounting accuracy and efficiency. First, institutions should maintain centralized bond databases that store all CUSIP-level information, including bond balances, interest rates, payment schedules, and maturity dates.

Second, institutions should automate bond tracking and accounting processes whenever possible. Automation reduces manual errors and improves reporting accuracy. Third, regular reconciliation should be performed to ensure that accounting records match trustee and custodian reports.

Fourth, institutions should maintain detailed documentation and audit trails for all bond transactions and accounting entries. This helps during audits and regulatory reviews. Finally, accounting teams should regularly review bond valuations, income calculations, and cash flow allocations to ensure accuracy.

Future Trends in Securitization Bond Accounting

The future of securitization cusip bond accounting will likely involve increased automation, improved data analytics, and better integration between accounting and portfolio management systems. Financial institutions are investing in advanced software solutions that can track bonds in real time and generate detailed financial reports automatically.

Data analytics tools are also being used to analyze bond performance, predict cash flows, and assess risk exposure. These tools rely heavily on accurate CUSIP-level accounting data.

Blockchain technology may also play a role in the future of securitized bond tracking and accounting by providing secure and transparent transaction records. This could further improve transparency and reduce reconciliation issues in the securitization market.

As the securitization industry continues to evolve, accurate accounting, tracking, and reporting will remain essential. Institutions that implement strong securitization cusip bond accounting practices will be better positioned to manage risk, ensure compliance, and maintain accurate financial records in an increasingly complex financial environment.

Conclusion

In today’s complex financial environment, securitization cusip bond accounting plays a vital role in ensuring accurate bond tracking, transparent financial reporting, and regulatory compliance. As securitized instruments such as mortgage-backed securities and asset-backed securities continue to grow in volume and complexity, the need for precise accounting at the CUSIP level becomes increasingly important. Proper accounting practices help institutions track bond performance, manage cash flows, record interest income, and maintain accurate portfolio valuations.

Effective securitization cusip bond accounting also supports audit readiness, reconciliation accuracy, and risk management. By tracking each security using its unique CUSIP identifier, financial institutions can reduce reporting errors, improve transparency, and ensure that investors and stakeholders receive accurate financial information. This level of detail is essential for portfolio management, performance analysis, and regulatory reporting.

Organizations that implement strong systems, automation tools, and reconciliation processes for securitization cusip bond accounting can significantly improve operational efficiency and financial accuracy. As technology continues to evolve, automated bond tracking and reporting systems will further enhance the accuracy and reliability of securitized bond accounting.

Ultimately, accurate securitization cusip bond accounting is not just an accounting function—it is a critical component of financial transparency, compliance, and effective investment management in the modern securitization market.

Strengthen Your Cases with Expert Securitization & Forensic Audit Support

For over four years, Mortgage Audits Online has been a trusted partner for professionals who need accurate, detailed, and reliable securitization and forensic audit support. We specialize exclusively in business-to-business services, helping our associates build stronger, more effective cases with comprehensive research, analysis, and reporting.

Our team understands the complexities of securitization, CUSIP research, bond tracking, and forensic loan audits. We work closely with attorneys, auditors, financial professionals, and industry specialists to provide the documentation and insights needed to support case strategies and financial investigations. Our goal is to provide clear, well-organized audit reports and securitization research that can help strengthen your case preparation and improve your professional outcomes.

When accuracy, reliability, and professional support matter, Mortgage Audits Online is here to assist you. Partner with a team that understands the details, the documentation, and the importance of delivering precise information on time.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

Phone: 877-399-2995

Fax: 877-398-5288

Website: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”