In the modern financial world, structured finance and securitization have become essential tools for banks, lenders, and financial institutions to manage risk, improve liquidity, and distribute credit exposure. One of the most important components in this complex financial structure is securitization cusip bond accounting, which plays a critical role in tracking, reporting, and valuing securitized instruments under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). Understanding how securitization cusip bond accounting works is essential for financial professionals, auditors, forensic analysts, and legal experts who deal with mortgage-backed securities, asset-backed securities, and structured finance transactions.

Securitization involves pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into securities that are sold to investors. Each security issued in a securitization transaction is assigned a unique CUSIP number, which serves as an identification code used for tracking and reporting purposes. This is where securitization cusip bond accounting becomes crucial, because every tranche, bond class, and payment structure must be recorded, tracked, and reported accurately in financial statements and investor reports. Without proper securitization cusip bond accounting, it would be nearly impossible to track ownership, cash flows, bond performance, and compliance with accounting standards.

Under both GAAP and IFRS, securitized assets and related bonds must be accounted for based on whether the transfer qualifies as a sale or a secured borrowing. This determination affects how assets, liabilities, income recognition, and disclosures are recorded in financial statements. Securitization cusip bond accounting helps accountants and financial analysts identify each bond tranche separately, calculate interest income, amortization, impairments, and fair value adjustments. It also ensures transparency and compliance with financial reporting requirements, especially for complex structured finance transactions.

Another important aspect of securitization cusip bond accounting is the tracking of bond tranches such as senior, mezzanine, and subordinate classes. Each tranche has different risk levels, interest rates, maturity periods, and payment priorities. Accounting for these tranches requires detailed tracking of principal payments, interest income, servicing fees, and credit losses. Under GAAP, accounting rules such as ASC 860 (Transfers and Servicing) and ASC 320 (Investments – Debt Securities) govern how securitized bonds are recorded and reported. Under IFRS, standards such as IFRS 9 and IFRS 10 govern financial instruments, consolidation, and derecognition of financial assets. Proper securitization cusip bond accounting ensures compliance with these standards and accurate financial reporting.

In addition, securitization cusip bond accounting plays a significant role in forensic accounting, litigation support, and loan audits. Many financial investigations and securitization audits rely on CUSIP tracking to identify where loans were transferred, how bonds were issued, and whether accounting treatments were properly applied. By analyzing CUSIP-level bond data, auditors and analysts can trace cash flows, ownership transfers, and reporting discrepancies. This makes securitization cusip bond accounting not only an accounting function but also an investigative and compliance tool.

Furthermore, investors rely heavily on securitization cusip bond accounting for portfolio valuation, risk assessment, and investment reporting. Investment firms, hedge funds, pension funds, and insurance companies invest heavily in securitized bonds, and accurate accounting ensures proper valuation, income recognition, and disclosure. Any errors in securitization cusip bond accounting can lead to misstatement of financial statements, regulatory issues, and investor reporting errors.

Overall, securitization cusip bond accounting forms the backbone of financial reporting for structured finance and securitized instruments under both GAAP and IFRS. It ensures transparency, compliance, accurate reporting, and proper tracking of securitized bonds and cash flows. As securitization markets continue to grow globally, the importance of securitization cusip bond accounting will continue to increase, especially for financial institutions, auditors, and forensic accounting professionals involved in structured finance transactions.

Understanding the Structure of Securitization Before Accounting Treatment

To understand how securitization cusip bond accounting works under GAAP and IFRS, it is important to first understand the structure of a securitization transaction. Securitization begins when a financial institution, often called the originator, pools together financial assets such as mortgages, auto loans, credit card receivables, or business loans. These pooled assets are then transferred to a Special Purpose Vehicle (SPV) or Special Purpose Entity (SPE), which is legally separate from the originator. The SPV then issues bonds or securities to investors, and each of these securities is assigned a unique CUSIP number for identification and tracking.

This is where securitization cusip bond accounting becomes essential because each tranche of bonds issued by the SPV must be tracked individually. These tranches may include senior bonds, mezzanine bonds, and subordinate bonds, each with different risk levels, interest rates, and payment priorities. Accounting systems must track each CUSIP separately for interest income, principal payments, amortization, impairments, and fair value adjustments. Without proper securitization cusip bond accounting, financial reporting for securitized instruments would be inaccurate and non-compliant with accounting standards.

Under both GAAP and IFRS, the accounting treatment depends heavily on whether the securitization is treated as a sale or as a secured borrowing. This classification determines whether the assets are removed from the balance sheet or remain on the balance sheet of the originator. Therefore, securitization cusip bond accounting is closely tied to asset derecognition rules, consolidation rules, and financial instrument classification.

GAAP Accounting Treatment for Securitized Bonds and CUSIP Tracking

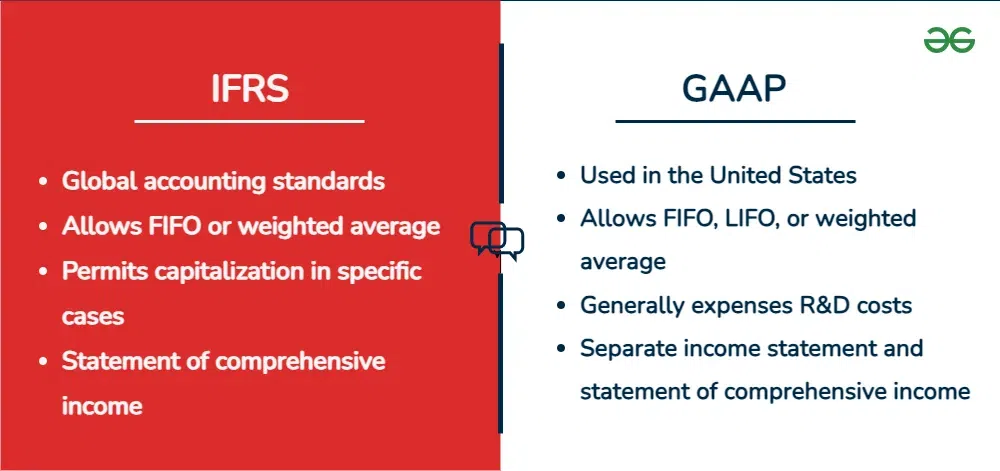

Under GAAP, securitization accounting is mainly governed by ASC 860 (Transfers and Servicing) and ASC 320 (Investments in Debt Securities). These standards determine whether a transfer of financial assets qualifies as a true sale or should be treated as a secured borrowing. If the transfer qualifies as a sale, the originator removes the assets from its balance sheet and recognizes any gain or loss on sale. If it does not qualify as a sale, the assets remain on the balance sheet and the proceeds are recorded as a liability.

In this process, securitization cusip bond accounting is used to track each bond issued in the securitization structure. Each CUSIP represents a specific tranche of bonds, and accounting entries must be recorded separately for each tranche. Interest income must be recorded based on the effective interest rate method, and principal payments must reduce the carrying value of the investment. If the bonds are classified as Available for Sale, they must be marked to fair value with unrealized gains or losses recorded in Other Comprehensive Income. If classified as Trading Securities, gains and losses are recorded in the income statement.

Another important area where securitization cusip bond accounting is used under GAAP is impairment analysis. If the value of securitized bonds declines due to credit losses or market changes, impairment must be recognized according to accounting standards. This requires tracking each bond by its CUSIP to determine whether the impairment is temporary or other-than-temporary. Therefore, accurate securitization cusip bond accounting ensures proper valuation, impairment recognition, and financial reporting.

IFRS Accounting Treatment for Securitization and Bond Reporting

Under IFRS, securitization accounting is governed primarily by IFRS 9 (Financial Instruments) and IFRS 10 (Consolidated Financial Statements). IFRS focuses heavily on control, risk transfer, and the business model test when determining whether securitized assets should be derecognized from the balance sheet. If the originator transfers substantially all risks and rewards, the assets can be removed from the balance sheet. If not, the assets remain on the balance sheet and the transaction is treated as financing.

In IFRS reporting, securitization cusip bond accounting is used to classify securitized bonds into categories such as amortized cost, fair value through profit and loss (FVTPL), or fair value through other comprehensive income (FVOCI). Each bond identified by its CUSIP must be evaluated based on cash flow characteristics and business model classification. Interest income is recorded using the effective interest method, and bonds measured at fair value must be revalued at each reporting period.

Impairment accounting under IFRS also relies heavily on securitization cusip bond accounting because IFRS uses the Expected Credit Loss (ECL) model. This means companies must estimate future credit losses on securitized bonds and record allowances accordingly. Since each bond tranche has different risk levels, the Expected Credit Loss must be calculated separately for each CUSIP. This makes securitization cusip bond accounting extremely important for IFRS financial reporting and risk management.

Importance of CUSIP-Level Tracking in Financial Reporting and Compliance

One of the most important functions of securitization cusip bond accounting is CUSIP-level tracking. Each securitized bond has its own interest rate, maturity date, payment structure, and risk profile. Therefore, accounting cannot be done at a pool level only; it must also be done at the individual bond level. CUSIP tracking allows accountants and financial analysts to monitor bond performance, interest income, principal paydowns, and valuation changes.

CUSIP-level accounting is also critical for investor reporting. Investors receive monthly or quarterly reports showing cash flows, interest payments, and principal balances for each bond tranche. These reports rely on accurate securitization cusip bond accounting to ensure that investors are paid correctly and financial statements reflect accurate investment values.

Regulatory compliance is another major reason why securitization cusip bond accounting is important. Financial institutions must comply with SEC reporting requirements, bank regulatory reporting, and international financial reporting standards. Regulators often require detailed reporting of securitized assets and bond holdings at the CUSIP level. Any errors in securitization cusip bond accounting can result in financial restatements, regulatory penalties, or audit findings.

Role of Securitization CUSIP Bond Accounting in Forensic Audits and Litigation

Another major area where securitization cusip bond accounting is used is forensic accounting and securitization audits. In many legal and financial investigations, auditors analyze securitization structures to determine ownership of loans, cash flow distributions, and accounting treatment of securitized assets. By tracing bonds through their CUSIP numbers, forensic accountants can identify where loans were transferred, how securities were issued, and whether accounting entries were recorded properly.

For example, in mortgage securitization investigations, analysts often track mortgage loans through securitization pools and then track the bonds issued from those pools using CUSIP numbers. This process relies heavily on securitization cusip bond accounting records, investor reports, trustee reports, and payment distribution reports. Without accurate accounting records tied to CUSIP numbers, forensic analysis would be extremely difficult.

Litigation support professionals also rely on securitization cusip bond accounting when analyzing financial damages, misrepresentation claims, or securitization reporting errors. Courts often require detailed financial tracing, and CUSIP-level accounting records provide the necessary documentation and audit trail.

Differences Between GAAP and IFRS in Securitization Bond Accounting

Although both GAAP and IFRS cover securitization accounting, there are important differences in how securitization cusip bond accounting is applied. GAAP focuses more on legal isolation and transfer of control when determining whether assets can be removed from the balance sheet. IFRS focuses more on risk and reward transfer and control over the SPV.

Another difference is impairment accounting. GAAP uses a credit loss model that differs from the IFRS Expected Credit Loss model. Under IFRS, companies must recognize expected losses earlier, which means securitization cusip bond accounting under IFRS often involves more frequent impairment calculations and valuation adjustments.

Fair value measurement is also handled differently in some cases, which can lead to different bond valuations under GAAP and IFRS. Despite these differences, both accounting frameworks require detailed bond tracking, interest income calculation, and disclosure reporting, all of which depend on accurate securitization cusip bond accounting.

Conclusion

How Securitization CUSIP Bond Accounting Works Under GAAP and IFRS

In summary, securitization cusip bond accounting is a critical component of structured finance accounting and financial reporting. It allows financial institutions, investors, auditors, and regulators to track securitized bonds, record interest income, monitor principal payments, calculate impairments, and ensure compliance with GAAP and IFRS reporting standards. Whether under GAAP or IFRS, the core purpose of securitization cusip bond accounting remains the same: accurate tracking, reporting, valuation, and compliance for securitized bonds and structured finance instruments.

As securitization markets continue to grow and structured finance transactions become more complex, the importance of securitization cusip bond accounting will continue to increase. Financial professionals who understand CUSIP-level accounting, securitization structures, and GAAP and IFRS reporting requirements will be better equipped to handle complex financial instruments, regulatory reporting, forensic audits, and structured finance accounting challenges.

Build Stronger Cases with Trusted Securitization & Forensic Audit Experts

For over four years, we have been helping our associates and business partners build stronger, more accurate, and well-documented cases through professional securitization analysis and forensic audits. Our expertise in securitization research, CUSIP analysis, bond tracking, and forensic loan auditing allows our partners to strengthen litigation support, compliance reviews, and financial investigations with reliable data and detailed reporting.

We are proud to operate exclusively as a business-to-business provider, supporting attorneys, auditors, forensic analysts, mortgage professionals, and financial service companies with specialized securitization and CUSIP research services. Our goal is to provide accurate, timely, and professional reports that help our associates make informed decisions and build stronger case strategies.

If you are looking for a reliable partner in securitization audits, forensic loan analysis, or CUSIP bond research, our team is ready to support your business with professional expertise and dependable service.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

In the modern financial world, structured finance and securitization have become essential tools for banks, lenders, and financial institutions to manage risk, improve liquidity, and distribute credit exposure. One of the most important components in this complex financial structure is securitization cusip bond accounting, which plays a critical role in tracking, reporting, and valuing securitized instruments under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). Understanding how securitization cusip bond accounting works is essential for financial professionals, auditors, forensic analysts, and legal experts who deal with mortgage-backed securities, asset-backed securities, and structured finance transactions.

Securitization involves pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into securities that are sold to investors. Each security issued in a securitization transaction is assigned a unique CUSIP number, which serves as an identification code used for tracking and reporting purposes. This is where securitization cusip bond accounting becomes crucial, because every tranche, bond class, and payment structure must be recorded, tracked, and reported accurately in financial statements and investor reports. Without proper securitization cusip bond accounting, it would be nearly impossible to track ownership, cash flows, bond performance, and compliance with accounting standards.

Under both GAAP and IFRS, securitized assets and related bonds must be accounted for based on whether the transfer qualifies as a sale or a secured borrowing. This determination affects how assets, liabilities, income recognition, and disclosures are recorded in financial statements. Securitization cusip bond accounting helps accountants and financial analysts identify each bond tranche separately, calculate interest income, amortization, impairments, and fair value adjustments. It also ensures transparency and compliance with financial reporting requirements, especially for complex structured finance transactions.

Another important aspect of securitization cusip bond accounting is the tracking of bond tranches such as senior, mezzanine, and subordinate classes. Each tranche has different risk levels, interest rates, maturity periods, and payment priorities. Accounting for these tranches requires detailed tracking of principal payments, interest income, servicing fees, and credit losses. Under GAAP, accounting rules such as ASC 860 (Transfers and Servicing) and ASC 320 (Investments – Debt Securities) govern how securitized bonds are recorded and reported. Under IFRS, standards such as IFRS 9 and IFRS 10 govern financial instruments, consolidation, and derecognition of financial assets. Proper securitization cusip bond accounting ensures compliance with these standards and accurate financial reporting.

In addition, securitization cusip bond accounting plays a significant role in forensic accounting, litigation support, and loan audits. Many financial investigations and securitization audits rely on CUSIP tracking to identify where loans were transferred, how bonds were issued, and whether accounting treatments were properly applied. By analyzing CUSIP-level bond data, auditors and analysts can trace cash flows, ownership transfers, and reporting discrepancies. This makes securitization cusip bond accounting not only an accounting function but also an investigative and compliance tool.

Furthermore, investors rely heavily on securitization cusip bond accounting for portfolio valuation, risk assessment, and investment reporting. Investment firms, hedge funds, pension funds, and insurance companies invest heavily in securitized bonds, and accurate accounting ensures proper valuation, income recognition, and disclosure. Any errors in securitization cusip bond accounting can lead to misstatement of financial statements, regulatory issues, and investor reporting errors.

Overall, securitization cusip bond accounting forms the backbone of financial reporting for structured finance and securitized instruments under both GAAP and IFRS. It ensures transparency, compliance, accurate reporting, and proper tracking of securitized bonds and cash flows. As securitization markets continue to grow globally, the importance of securitization cusip bond accounting will continue to increase, especially for financial institutions, auditors, and forensic accounting professionals involved in structured finance transactions.

Understanding the Structure of Securitization Before Accounting Treatment

To understand how securitization cusip bond accounting works under GAAP and IFRS, it is important to first understand the structure of a securitization transaction. Securitization begins when a financial institution, often called the originator, pools together financial assets such as mortgages, auto loans, credit card receivables, or business loans. These pooled assets are then transferred to a Special Purpose Vehicle (SPV) or Special Purpose Entity (SPE), which is legally separate from the originator. The SPV then issues bonds or securities to investors, and each of these securities is assigned a unique CUSIP number for identification and tracking.

This is where securitization cusip bond accounting becomes essential because each tranche of bonds issued by the SPV must be tracked individually. These tranches may include senior bonds, mezzanine bonds, and subordinate bonds, each with different risk levels, interest rates, and payment priorities. Accounting systems must track each CUSIP separately for interest income, principal payments, amortization, impairments, and fair value adjustments. Without proper securitization cusip bond accounting, financial reporting for securitized instruments would be inaccurate and non-compliant with accounting standards.

Under both GAAP and IFRS, the accounting treatment depends heavily on whether the securitization is treated as a sale or as a secured borrowing. This classification determines whether the assets are removed from the balance sheet or remain on the balance sheet of the originator. Therefore, securitization cusip bond accounting is closely tied to asset derecognition rules, consolidation rules, and financial instrument classification.

GAAP Accounting Treatment for Securitized Bonds and CUSIP Tracking

Under GAAP, securitization accounting is mainly governed by ASC 860 (Transfers and Servicing) and ASC 320 (Investments in Debt Securities). These standards determine whether a transfer of financial assets qualifies as a true sale or should be treated as a secured borrowing. If the transfer qualifies as a sale, the originator removes the assets from its balance sheet and recognizes any gain or loss on sale. If it does not qualify as a sale, the assets remain on the balance sheet and the proceeds are recorded as a liability.

In this process, securitization cusip bond accounting is used to track each bond issued in the securitization structure. Each CUSIP represents a specific tranche of bonds, and accounting entries must be recorded separately for each tranche. Interest income must be recorded based on the effective interest rate method, and principal payments must reduce the carrying value of the investment. If the bonds are classified as Available for Sale, they must be marked to fair value with unrealized gains or losses recorded in Other Comprehensive Income. If classified as Trading Securities, gains and losses are recorded in the income statement.

Another important area where securitization cusip bond accounting is used under GAAP is impairment analysis. If the value of securitized bonds declines due to credit losses or market changes, impairment must be recognized according to accounting standards. This requires tracking each bond by its CUSIP to determine whether the impairment is temporary or other-than-temporary. Therefore, accurate securitization cusip bond accounting ensures proper valuation, impairment recognition, and financial reporting.

IFRS Accounting Treatment for Securitization and Bond Reporting

Under IFRS, securitization accounting is governed primarily by IFRS 9 (Financial Instruments) and IFRS 10 (Consolidated Financial Statements). IFRS focuses heavily on control, risk transfer, and the business model test when determining whether securitized assets should be derecognized from the balance sheet. If the originator transfers substantially all risks and rewards, the assets can be removed from the balance sheet. If not, the assets remain on the balance sheet and the transaction is treated as financing.

In IFRS reporting, securitization cusip bond accounting is used to classify securitized bonds into categories such as amortized cost, fair value through profit and loss (FVTPL), or fair value through other comprehensive income (FVOCI). Each bond identified by its CUSIP must be evaluated based on cash flow characteristics and business model classification. Interest income is recorded using the effective interest method, and bonds measured at fair value must be revalued at each reporting period.

Impairment accounting under IFRS also relies heavily on securitization cusip bond accounting because IFRS uses the Expected Credit Loss (ECL) model. This means companies must estimate future credit losses on securitized bonds and record allowances accordingly. Since each bond tranche has different risk levels, the Expected Credit Loss must be calculated separately for each CUSIP. This makes securitization cusip bond accounting extremely important for IFRS financial reporting and risk management.

Importance of CUSIP-Level Tracking in Financial Reporting and Compliance

One of the most important functions of securitization cusip bond accounting is CUSIP-level tracking. Each securitized bond has its own interest rate, maturity date, payment structure, and risk profile. Therefore, accounting cannot be done at a pool level only; it must also be done at the individual bond level. CUSIP tracking allows accountants and financial analysts to monitor bond performance, interest income, principal paydowns, and valuation changes.

CUSIP-level accounting is also critical for investor reporting. Investors receive monthly or quarterly reports showing cash flows, interest payments, and principal balances for each bond tranche. These reports rely on accurate securitization cusip bond accounting to ensure that investors are paid correctly and financial statements reflect accurate investment values.

Regulatory compliance is another major reason why securitization cusip bond accounting is important. Financial institutions must comply with SEC reporting requirements, bank regulatory reporting, and international financial reporting standards. Regulators often require detailed reporting of securitized assets and bond holdings at the CUSIP level. Any errors in securitization cusip bond accounting can result in financial restatements, regulatory penalties, or audit findings.

Role of Securitization CUSIP Bond Accounting in Forensic Audits and Litigation

Another major area where securitization cusip bond accounting is used is forensic accounting and securitization audits. In many legal and financial investigations, auditors analyze securitization structures to determine ownership of loans, cash flow distributions, and accounting treatment of securitized assets. By tracing bonds through their CUSIP numbers, forensic accountants can identify where loans were transferred, how securities were issued, and whether accounting entries were recorded properly.

For example, in mortgage securitization investigations, analysts often track mortgage loans through securitization pools and then track the bonds issued from those pools using CUSIP numbers. This process relies heavily on securitization cusip bond accounting records, investor reports, trustee reports, and payment distribution reports. Without accurate accounting records tied to CUSIP numbers, forensic analysis would be extremely difficult.

Litigation support professionals also rely on securitization cusip bond accounting when analyzing financial damages, misrepresentation claims, or securitization reporting errors. Courts often require detailed financial tracing, and CUSIP-level accounting records provide the necessary documentation and audit trail.

Differences Between GAAP and IFRS in Securitization Bond Accounting

Although both GAAP and IFRS cover securitization accounting, there are important differences in how securitization cusip bond accounting is applied. GAAP focuses more on legal isolation and transfer of control when determining whether assets can be removed from the balance sheet. IFRS focuses more on risk and reward transfer and control over the SPV.

Another difference is impairment accounting. GAAP uses a credit loss model that differs from the IFRS Expected Credit Loss model. Under IFRS, companies must recognize expected losses earlier, which means securitization cusip bond accounting under IFRS often involves more frequent impairment calculations and valuation adjustments.

Fair value measurement is also handled differently in some cases, which can lead to different bond valuations under GAAP and IFRS. Despite these differences, both accounting frameworks require detailed bond tracking, interest income calculation, and disclosure reporting, all of which depend on accurate securitization cusip bond accounting.

Conclusion

How Securitization CUSIP Bond Accounting Works Under GAAP and IFRS

In summary, securitization cusip bond accounting is a critical component of structured finance accounting and financial reporting. It allows financial institutions, investors, auditors, and regulators to track securitized bonds, record interest income, monitor principal payments, calculate impairments, and ensure compliance with GAAP and IFRS reporting standards. Whether under GAAP or IFRS, the core purpose of securitization cusip bond accounting remains the same: accurate tracking, reporting, valuation, and compliance for securitized bonds and structured finance instruments.

As securitization markets continue to grow and structured finance transactions become more complex, the importance of securitization cusip bond accounting will continue to increase. Financial professionals who understand CUSIP-level accounting, securitization structures, and GAAP and IFRS reporting requirements will be better equipped to handle complex financial instruments, regulatory reporting, forensic audits, and structured finance accounting challenges.

Build Stronger Cases with Trusted Securitization & Forensic Audit Experts

For over four years, we have been helping our associates and business partners build stronger, more accurate, and well-documented cases through professional securitization analysis and forensic audits. Our expertise in securitization research, CUSIP analysis, bond tracking, and forensic loan auditing allows our partners to strengthen litigation support, compliance reviews, and financial investigations with reliable data and detailed reporting.

We are proud to operate exclusively as a business-to-business provider, supporting attorneys, auditors, forensic analysts, mortgage professionals, and financial service companies with specialized securitization and CUSIP research services. Our goal is to provide accurate, timely, and professional reports that help our associates make informed decisions and build stronger case strategies.

If you are looking for a reliable partner in securitization audits, forensic loan analysis, or CUSIP bond research, our team is ready to support your business with professional expertise and dependable service.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

In the modern financial world, structured finance and securitization have become essential tools for banks, lenders, and financial institutions to manage risk, improve liquidity, and distribute credit exposure. One of the most important components in this complex financial structure is securitization cusip bond accounting, which plays a critical role in tracking, reporting, and valuing securitized instruments under both GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). Understanding how securitization cusip bond accounting works is essential for financial professionals, auditors, forensic analysts, and legal experts who deal with mortgage-backed securities, asset-backed securities, and structured finance transactions.

Securitization involves pooling financial assets such as mortgages, auto loans, credit card receivables, or student loans and converting them into securities that are sold to investors. Each security issued in a securitization transaction is assigned a unique CUSIP number, which serves as an identification code used for tracking and reporting purposes. This is where securitization cusip bond accounting becomes crucial, because every tranche, bond class, and payment structure must be recorded, tracked, and reported accurately in financial statements and investor reports. Without proper securitization cusip bond accounting, it would be nearly impossible to track ownership, cash flows, bond performance, and compliance with accounting standards.

Under both GAAP and IFRS, securitized assets and related bonds must be accounted for based on whether the transfer qualifies as a sale or a secured borrowing. This determination affects how assets, liabilities, income recognition, and disclosures are recorded in financial statements. Securitization cusip bond accounting helps accountants and financial analysts identify each bond tranche separately, calculate interest income, amortization, impairments, and fair value adjustments. It also ensures transparency and compliance with financial reporting requirements, especially for complex structured finance transactions.

Another important aspect of securitization cusip bond accounting is the tracking of bond tranches such as senior, mezzanine, and subordinate classes. Each tranche has different risk levels, interest rates, maturity periods, and payment priorities. Accounting for these tranches requires detailed tracking of principal payments, interest income, servicing fees, and credit losses. Under GAAP, accounting rules such as ASC 860 (Transfers and Servicing) and ASC 320 (Investments – Debt Securities) govern how securitized bonds are recorded and reported. Under IFRS, standards such as IFRS 9 and IFRS 10 govern financial instruments, consolidation, and derecognition of financial assets. Proper securitization cusip bond accounting ensures compliance with these standards and accurate financial reporting.

In addition, securitization cusip bond accounting plays a significant role in forensic accounting, litigation support, and loan audits. Many financial investigations and securitization audits rely on CUSIP tracking to identify where loans were transferred, how bonds were issued, and whether accounting treatments were properly applied. By analyzing CUSIP-level bond data, auditors and analysts can trace cash flows, ownership transfers, and reporting discrepancies. This makes securitization cusip bond accounting not only an accounting function but also an investigative and compliance tool.

Furthermore, investors rely heavily on securitization cusip bond accounting for portfolio valuation, risk assessment, and investment reporting. Investment firms, hedge funds, pension funds, and insurance companies invest heavily in securitized bonds, and accurate accounting ensures proper valuation, income recognition, and disclosure. Any errors in securitization cusip bond accounting can lead to misstatement of financial statements, regulatory issues, and investor reporting errors.

Overall, securitization cusip bond accounting forms the backbone of financial reporting for structured finance and securitized instruments under both GAAP and IFRS. It ensures transparency, compliance, accurate reporting, and proper tracking of securitized bonds and cash flows. As securitization markets continue to grow globally, the importance of securitization cusip bond accounting will continue to increase, especially for financial institutions, auditors, and forensic accounting professionals involved in structured finance transactions.

Understanding the Structure of Securitization Before Accounting Treatment

To understand how securitization cusip bond accounting works under GAAP and IFRS, it is important to first understand the structure of a securitization transaction. Securitization begins when a financial institution, often called the originator, pools together financial assets such as mortgages, auto loans, credit card receivables, or business loans. These pooled assets are then transferred to a Special Purpose Vehicle (SPV) or Special Purpose Entity (SPE), which is legally separate from the originator. The SPV then issues bonds or securities to investors, and each of these securities is assigned a unique CUSIP number for identification and tracking.

This is where securitization cusip bond accounting becomes essential because each tranche of bonds issued by the SPV must be tracked individually. These tranches may include senior bonds, mezzanine bonds, and subordinate bonds, each with different risk levels, interest rates, and payment priorities. Accounting systems must track each CUSIP separately for interest income, principal payments, amortization, impairments, and fair value adjustments. Without proper securitization cusip bond accounting, financial reporting for securitized instruments would be inaccurate and non-compliant with accounting standards.

Under both GAAP and IFRS, the accounting treatment depends heavily on whether the securitization is treated as a sale or as a secured borrowing. This classification determines whether the assets are removed from the balance sheet or remain on the balance sheet of the originator. Therefore, securitization cusip bond accounting is closely tied to asset derecognition rules, consolidation rules, and financial instrument classification.

GAAP Accounting Treatment for Securitized Bonds and CUSIP Tracking

Under GAAP, securitization accounting is mainly governed by ASC 860 (Transfers and Servicing) and ASC 320 (Investments in Debt Securities). These standards determine whether a transfer of financial assets qualifies as a true sale or should be treated as a secured borrowing. If the transfer qualifies as a sale, the originator removes the assets from its balance sheet and recognizes any gain or loss on sale. If it does not qualify as a sale, the assets remain on the balance sheet and the proceeds are recorded as a liability.

In this process, securitization cusip bond accounting is used to track each bond issued in the securitization structure. Each CUSIP represents a specific tranche of bonds, and accounting entries must be recorded separately for each tranche. Interest income must be recorded based on the effective interest rate method, and principal payments must reduce the carrying value of the investment. If the bonds are classified as Available for Sale, they must be marked to fair value with unrealized gains or losses recorded in Other Comprehensive Income. If classified as Trading Securities, gains and losses are recorded in the income statement.

Another important area where securitization cusip bond accounting is used under GAAP is impairment analysis. If the value of securitized bonds declines due to credit losses or market changes, impairment must be recognized according to accounting standards. This requires tracking each bond by its CUSIP to determine whether the impairment is temporary or other-than-temporary. Therefore, accurate securitization cusip bond accounting ensures proper valuation, impairment recognition, and financial reporting.

IFRS Accounting Treatment for Securitization and Bond Reporting

Under IFRS, securitization accounting is governed primarily by IFRS 9 (Financial Instruments) and IFRS 10 (Consolidated Financial Statements). IFRS focuses heavily on control, risk transfer, and the business model test when determining whether securitized assets should be derecognized from the balance sheet. If the originator transfers substantially all risks and rewards, the assets can be removed from the balance sheet. If not, the assets remain on the balance sheet and the transaction is treated as financing.

In IFRS reporting, securitization cusip bond accounting is used to classify securitized bonds into categories such as amortized cost, fair value through profit and loss (FVTPL), or fair value through other comprehensive income (FVOCI). Each bond identified by its CUSIP must be evaluated based on cash flow characteristics and business model classification. Interest income is recorded using the effective interest method, and bonds measured at fair value must be revalued at each reporting period.

Impairment accounting under IFRS also relies heavily on securitization cusip bond accounting because IFRS uses the Expected Credit Loss (ECL) model. This means companies must estimate future credit losses on securitized bonds and record allowances accordingly. Since each bond tranche has different risk levels, the Expected Credit Loss must be calculated separately for each CUSIP. This makes securitization cusip bond accounting extremely important for IFRS financial reporting and risk management.

Importance of CUSIP-Level Tracking in Financial Reporting and Compliance

One of the most important functions of securitization cusip bond accounting is CUSIP-level tracking. Each securitized bond has its own interest rate, maturity date, payment structure, and risk profile. Therefore, accounting cannot be done at a pool level only; it must also be done at the individual bond level. CUSIP tracking allows accountants and financial analysts to monitor bond performance, interest income, principal paydowns, and valuation changes.

CUSIP-level accounting is also critical for investor reporting. Investors receive monthly or quarterly reports showing cash flows, interest payments, and principal balances for each bond tranche. These reports rely on accurate securitization cusip bond accounting to ensure that investors are paid correctly and financial statements reflect accurate investment values.

Regulatory compliance is another major reason why securitization cusip bond accounting is important. Financial institutions must comply with SEC reporting requirements, bank regulatory reporting, and international financial reporting standards. Regulators often require detailed reporting of securitized assets and bond holdings at the CUSIP level. Any errors in securitization cusip bond accounting can result in financial restatements, regulatory penalties, or audit findings.

Role of Securitization CUSIP Bond Accounting in Forensic Audits and Litigation

Another major area where securitization cusip bond accounting is used is forensic accounting and securitization audits. In many legal and financial investigations, auditors analyze securitization structures to determine ownership of loans, cash flow distributions, and accounting treatment of securitized assets. By tracing bonds through their CUSIP numbers, forensic accountants can identify where loans were transferred, how securities were issued, and whether accounting entries were recorded properly.

For example, in mortgage securitization investigations, analysts often track mortgage loans through securitization pools and then track the bonds issued from those pools using CUSIP numbers. This process relies heavily on securitization cusip bond accounting records, investor reports, trustee reports, and payment distribution reports. Without accurate accounting records tied to CUSIP numbers, forensic analysis would be extremely difficult.

Litigation support professionals also rely on securitization cusip bond accounting when analyzing financial damages, misrepresentation claims, or securitization reporting errors. Courts often require detailed financial tracing, and CUSIP-level accounting records provide the necessary documentation and audit trail.

Differences Between GAAP and IFRS in Securitization Bond Accounting

Although both GAAP and IFRS cover securitization accounting, there are important differences in how securitization cusip bond accounting is applied. GAAP focuses more on legal isolation and transfer of control when determining whether assets can be removed from the balance sheet. IFRS focuses more on risk and reward transfer and control over the SPV.

Another difference is impairment accounting. GAAP uses a credit loss model that differs from the IFRS Expected Credit Loss model. Under IFRS, companies must recognize expected losses earlier, which means securitization cusip bond accounting under IFRS often involves more frequent impairment calculations and valuation adjustments.

Fair value measurement is also handled differently in some cases, which can lead to different bond valuations under GAAP and IFRS. Despite these differences, both accounting frameworks require detailed bond tracking, interest income calculation, and disclosure reporting, all of which depend on accurate securitization cusip bond accounting.

Conclusion

How Securitization CUSIP Bond Accounting Works Under GAAP and IFRS

In summary, securitization cusip bond accounting is a critical component of structured finance accounting and financial reporting. It allows financial institutions, investors, auditors, and regulators to track securitized bonds, record interest income, monitor principal payments, calculate impairments, and ensure compliance with GAAP and IFRS reporting standards. Whether under GAAP or IFRS, the core purpose of securitization cusip bond accounting remains the same: accurate tracking, reporting, valuation, and compliance for securitized bonds and structured finance instruments.

As securitization markets continue to grow and structured finance transactions become more complex, the importance of securitization cusip bond accounting will continue to increase. Financial professionals who understand CUSIP-level accounting, securitization structures, and GAAP and IFRS reporting requirements will be better equipped to handle complex financial instruments, regulatory reporting, forensic audits, and structured finance accounting challenges.

Build Stronger Cases with Trusted Securitization & Forensic Audit Experts

For over four years, we have been helping our associates and business partners build stronger, more accurate, and well-documented cases through professional securitization analysis and forensic audits. Our expertise in securitization research, CUSIP analysis, bond tracking, and forensic loan auditing allows our partners to strengthen litigation support, compliance reviews, and financial investigations with reliable data and detailed reporting.

We are proud to operate exclusively as a business-to-business provider, supporting attorneys, auditors, forensic analysts, mortgage professionals, and financial service companies with specialized securitization and CUSIP research services. Our goal is to provide accurate, timely, and professional reports that help our associates make informed decisions and build stronger case strategies.

If you are looking for a reliable partner in securitization audits, forensic loan analysis, or CUSIP bond research, our team is ready to support your business with professional expertise and dependable service.

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”