In today’s structured finance environment, securitization cusip bond accounting has become an essential component of financial reporting, bond tracking, and compliance management for institutions involved in mortgage-backed securities, asset-backed securities, and other structured financial instruments. As financial markets continue to evolve, the complexity of securitization transactions has increased significantly, requiring more advanced accounting systems, precise CUSIP-level tracking, and strict regulatory reporting procedures. Organizations that manage securitized assets must maintain accurate records at the bond level to ensure transparency, compliance, and proper financial reporting. This is where securitization cusip bond accounting plays a critical role in the financial infrastructure of modern lending and investment institutions.

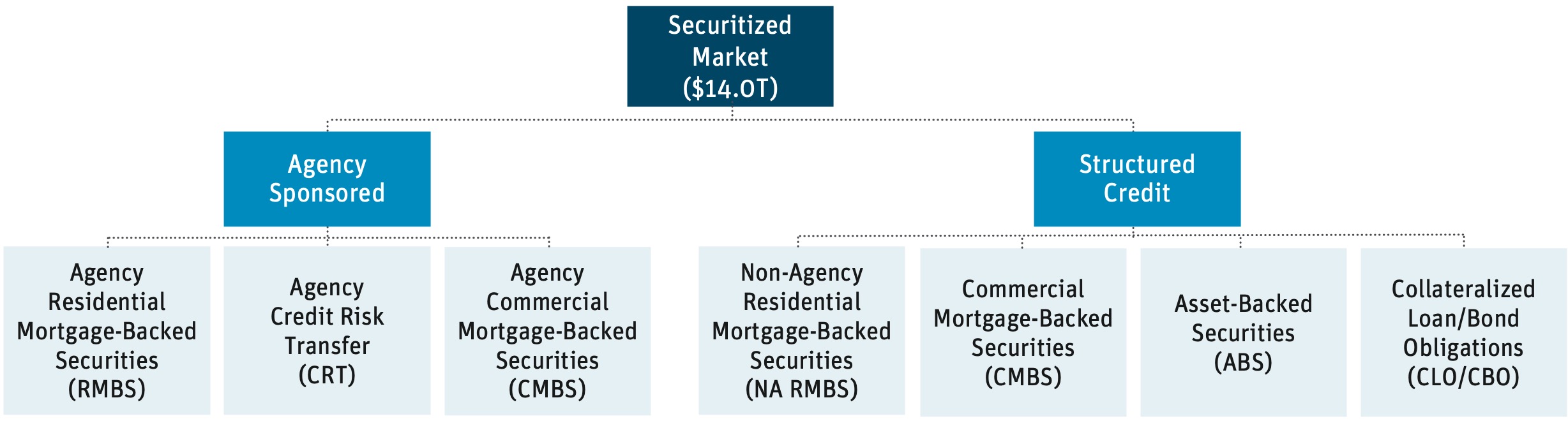

Securitization involves pooling financial assets such as mortgages, auto loans, credit card receivables, or other debt instruments and converting them into tradable securities. Each security issued from a securitization trust is assigned a unique CUSIP number, which acts as an identifier for tracking the bond in financial markets, accounting systems, and investor reporting platforms. Proper securitization cusip bond accounting ensures that every bond tranche is accounted for individually, including principal balances, interest payments, amortization schedules, and investor distributions. Without accurate CUSIP-level accounting, financial institutions may face reporting discrepancies, compliance risks, and reconciliation errors that can significantly impact financial statements and investor confidence.

One of the most important aspects of securitization cusip bond accounting is the ability to track bond performance over time. Each CUSIP represents a specific tranche with its own interest rate, maturity date, payment priority, and risk profile. Accounting systems must therefore be capable of handling multiple tranches within a single securitization structure, allocating payments correctly, and maintaining accurate amortization and interest accrual records. Advanced accounting platforms integrate loan-level data with bond-level reporting to ensure that cash flows from underlying assets are properly distributed to the corresponding bondholders. This integration is essential for accurate financial reporting and investor disclosures.

Another critical component of securitization cusip bond accounting is compliance and regulatory reporting. Financial institutions must comply with various accounting standards and reporting frameworks, including GAAP, IFRS, and regulatory requirements related to structured finance disclosures. Proper accounting at the CUSIP level helps organizations generate accurate reports for auditors, regulators, investors, and internal management. These reports may include bond balances, interest income, principal payments, gain or loss on sale, servicing fees, and trust performance metrics. Without a structured accounting system designed specifically for securitization, managing these reporting requirements can become extremely difficult and error-prone.

Technology and automation have significantly improved the efficiency of securitization cusip bond accounting systems. Modern structured finance accounting platforms can automatically reconcile loan pools, calculate bond payments, generate investor reports, and maintain CUSIP-level accounting records. Automation reduces manual errors, improves reporting accuracy, and ensures that financial data is consistent across accounting systems, servicing platforms, and trustee reports. Institutions that implement automated securitization accounting systems often experience improved operational efficiency, better compliance management, and more reliable financial reporting.

Risk management is another major reason why securitization cusip bond accounting is so important. Investors, auditors, and regulators require transparency into bond performance, cash flow allocations, and trust asset performance. Accurate accounting records at the CUSIP level allow organizations to analyze bond performance, monitor delinquency and default rates, and evaluate the financial health of securitization trusts. This level of transparency is essential for maintaining investor confidence and ensuring that securitization transactions remain compliant with financial regulations and reporting standards.

In summary, securitization cusip bond accounting is not just an accounting function but a critical financial management and reporting system that supports structured finance operations, investor reporting, compliance requirements, and risk management. As securitization structures become more complex and regulatory oversight continues to increase, organizations must implement advanced accounting systems and reporting strategies to manage securitized bonds effectively at the CUSIP level. Proper accounting, reporting, and compliance practices ensure transparency, accuracy, and financial stability within securitization transactions, making securitization cusip bond accounting an essential part of modern structured finance and bond management operations.

The Role of Structured Finance Systems in Securitization CUSIP Bond Accounting

Modern structured finance transactions involve thousands of loans, multiple bond tranches, complex payment waterfalls, and detailed investor reporting requirements. Because of this complexity, securitization cusip bond accounting cannot be handled using basic accounting software or simple spreadsheets. Instead, financial institutions rely on specialized structured finance accounting systems designed to track bonds at the CUSIP level, manage cash flow allocations, and generate investor and regulatory reports. These systems integrate loan servicing data, trustee reports, and bond payment schedules into a centralized accounting environment, ensuring that every tranche is accurately recorded and reconciled.

Structured finance accounting systems are designed to handle principal and interest allocations according to the securitization waterfall structure. Each CUSIP represents a bond tranche with its own priority of payment, interest rate, maturity date, and balance. The accounting system must calculate interest accruals, allocate principal payments, record servicing fees, and track reserve accounts. This is why securitization cusip bond accounting requires highly specialized software capable of handling tranche-level accounting rather than just pool-level accounting. Without these systems, it would be extremely difficult to maintain accurate financial records and investor reports.

Another important function of structured finance systems is reconciliation. Accounting teams must reconcile loan pool balances, bond balances, and trustee reports on a regular basis. Any discrepancy between loan balances and bond balances can create financial reporting errors and compliance issues. Through automated reconciliation tools, securitization cusip bond accounting systems help identify differences between servicing data and bond accounting records, allowing accounting teams to resolve discrepancies quickly and maintain accurate financial reporting.

Investor Reporting and Financial Statement Impact

Investor reporting is one of the most critical components of securitization cusip bond accounting because investors rely on accurate reports to evaluate bond performance, cash flow distributions, and trust asset performance. Investor reports typically include principal payments, interest payments, outstanding bond balances, delinquency rates, prepayment rates, and loss information. All of this information must be calculated and reported at the CUSIP level, which makes accurate accounting essential for investor transparency.

From a financial statement perspective, securitization accounting affects multiple areas of a company’s financial reports. These include interest income, servicing income, gain or loss on securitization, bond liabilities, trust assets, and reserve accounts. Proper securitization cusip bond accounting ensures that these financial statement items are recorded accurately and in compliance with accounting standards. If bond balances or interest calculations are incorrect, financial statements may be misstated, which can lead to audit issues or regulatory concerns.

Accounting teams must also track amortization of bond premiums and discounts, interest accruals, and deferred fees. These accounting entries are typically recorded at the CUSIP level because each bond tranche may have different pricing and yield characteristics. Accurate amortization schedules are therefore an essential part of securitization cusip bond accounting, ensuring that interest income and bond balances are reported correctly over time.

Compliance, Audit, and Regulatory Reporting Requirements

Compliance is another major reason why securitization cusip bond accounting is so important in structured finance. Financial institutions involved in securitization must comply with accounting standards such as GAAP or IFRS, as well as regulatory reporting requirements. Regulators and auditors often require detailed reports showing bond balances, cash flow allocations, interest income, and trust performance metrics at the CUSIP level.

During audits, auditors typically review bond accounting records, reconciliation reports, investor reports, and accounting policies related to securitization transactions. If accounting records are not maintained properly at the CUSIP level, the audit process can become complicated and may result in audit findings or financial statement adjustments. Proper securitization cusip bond accounting helps organizations maintain audit trails, transaction histories, and supporting documentation for all bond accounting entries.

Regulatory reporting may also require institutions to report securitized assets, bond liabilities, and trust performance metrics. These reports often rely on accurate CUSIP-level accounting data. Without a structured accounting system designed for securitization, generating these reports would be extremely difficult and time-consuming. This is why many financial institutions invest heavily in securitization accounting platforms and compliance reporting tools.

Cash Flow Waterfall and Tranche Accounting Complexity

One of the most complex areas of securitization cusip bond accounting is managing the cash flow waterfall. In securitization transactions, cash flows from underlying loans are distributed according to a specific priority structure known as the waterfall. Senior bond tranches are paid first, followed by mezzanine tranches, and then subordinate tranches. Each tranche has its own CUSIP number and payment priority.

Accounting for these cash flow allocations requires detailed calculations and accurate tracking of principal and interest payments. The accounting system must allocate cash flows correctly to each CUSIP and record the appropriate accounting entries for interest income, principal reduction, and bond balances. If cash flows are allocated incorrectly, bond balances and financial reports will be inaccurate. Therefore, managing the waterfall structure is one of the most important functions of securitization cusip bond accounting.

Additionally, some securitization structures include reserve accounts, overcollateralization accounts, and excess spread accounts. These accounts must also be tracked and recorded within the accounting system. The interaction between these accounts and bond payments adds another layer of complexity to securitization accounting, making specialized accounting systems essential.

Technology, Automation, and Data Integration

Technology plays a major role in modern securitization cusip bond accounting because manual accounting processes are no longer sufficient for managing complex securitization structures. Automated accounting systems can import loan servicing data, calculate bond payments, generate accounting entries, and produce investor reports automatically. Automation reduces errors, improves efficiency, and ensures consistency across financial reports.

Data integration is another important aspect of securitization accounting systems. Accounting systems must integrate with loan servicing platforms, trustee reporting systems, and general ledger systems. This integration ensures that loan balances, bond balances, and accounting records remain consistent across all systems. Proper data integration is essential for maintaining accurate financial records and ensuring that securitization cusip bond accounting processes run smoothly.

Automation also helps with monthly and quarterly reporting cycles. Accounting teams can generate investor reports, reconciliation reports, and financial statement reports much faster using automated systems. This improves operational efficiency and reduces the risk of reporting errors.

Risk Management and Portfolio Monitoring

Risk management is an important part of securitization cusip bond accounting because financial institutions must monitor bond performance, loan performance, and trust performance on an ongoing basis. Accounting records at the CUSIP level provide valuable information about bond balances, payment history, and performance trends. This information helps institutions evaluate credit risk, prepayment risk, and default risk associated with securitized assets.

Portfolio monitoring involves tracking delinquency rates, default rates, prepayment speeds, and loss severity. These metrics are often reported to investors and regulators and must be supported by accurate accounting records. By maintaining detailed accounting records at the CUSIP level, institutions can analyze bond performance and make informed financial and risk management decisions.

In complex securitization structures, risk exposure may vary significantly between different bond tranches. Senior tranches typically have lower risk, while subordinate tranches have higher risk but higher potential returns. Accurate securitization cusip bond accounting allows institutions to monitor the performance of each tranche separately and evaluate the overall risk profile of the securitization structure.

Operational Efficiency and Long-Term Financial Management

Efficient accounting processes are essential for organizations that manage multiple securitization transactions. Without proper systems and processes, accounting teams may spend excessive time reconciling data, preparing reports, and correcting errors. Implementing structured accounting systems and automation tools improves operational efficiency and reduces administrative costs.

Over the long term, securitization cusip bond accounting also supports financial planning and portfolio management. Accurate bond accounting records help organizations track income from securitization transactions, monitor bond balances, and evaluate the profitability of securitization programs. This information is important for financial planning, investment decisions, and business strategy.

As securitization markets continue to grow and structured finance transactions become more complex, the importance of accurate accounting at the CUSIP level will continue to increase. Organizations that invest in advanced accounting systems, automation tools, and strong accounting processes will be better positioned to manage securitization transactions, maintain compliance, and provide accurate financial reporting. This makes securitization cusip bond accounting a critical component of structured finance operations, financial reporting, and long-term financial management.

Conclusion

In the complex world of structured finance, securitization cusip bond accounting plays a critical role in ensuring accuracy, transparency, and compliance across all securitization transactions. From tracking bond tranches and managing cash flow waterfalls to generating investor reports and supporting regulatory compliance, proper accounting at the CUSIP level is essential for financial institutions, investors, and structured finance professionals. Without accurate securitization cusip bond accounting, organizations may face reconciliation issues, reporting errors, audit challenges, and compliance risks that can impact financial statements and investor confidence.

As securitization structures continue to evolve and become more sophisticated, the need for advanced accounting systems, automation tools, and integrated reporting platforms will continue to grow. Organizations that implement strong securitization cusip bond accounting processes are better equipped to manage bond performance, monitor risk, maintain accurate financial records, and meet regulatory reporting requirements. These accounting practices not only support day-to-day financial operations but also contribute to long-term financial management and strategic decision-making.

Ultimately, securitization cusip bond accounting is not just an accounting function but a foundational component of structured finance operations, ensuring that securitized bonds are properly tracked, reported, and managed throughout the life of the transaction.

Build Stronger Cases with Expert Securitization & Forensic Audit Support

If your organization relies on accurate securitization analysis, forensic loan reviews, and CUSIP research to support litigation, compliance, or financial investigations, having the right partner can make all the difference. For over four years, we have been dedicated to helping our associates build stronger, more detailed, and more defensible cases through professional securitization and forensic audit services. Our work is designed specifically for professionals who require accurate data, structured finance analysis, and reliable documentation to support complex financial cases.

We are exclusively a business-to-business provider, which means our services are built for attorneys, auditors, financial professionals, investigators, and organizations that need detailed securitization reports, CUSIP analysis, bond research, and forensic mortgage audits. Our experience, research capabilities, and structured finance knowledge allow us to provide the documentation and analysis needed to support case development, financial investigations, and securitization research.

Whether you are working on litigation support, forensic accounting, mortgage securitization research, or structured finance analysis, our team is committed to delivering accurate, professional, and timely reports that help strengthen your case and support your professional work.

Contact Information

Mortgage Audits Online

100 Rialto Place, Suite 700

Melbourne, FL 32901

📱 Phone: 877-399-2995

📠 Fax: 877-398-5288

🌐 Visit: https://cusipdata.com/

“Disclaimer Note: This article is for educational & entertainment purposes”